Nothing sedates rationality like large doses of effortless money

02 May 2024 _ News

‘The return of gravity’

The return of gravity

The second quarter begins with the return of the force of gravity on the markets. This force of gravity is related to the fact that the more expensive equity markets become in terms of valuations, the more sensitive they become to external factors. In this case the external factor that reminded us of the existence of the force of gravity is the US interest rate trend. In the chart below we see how the price-to-earnings ratio of the S&P500 (white line) fell from 21 to 19.8x PE (-6%), while the US ten-year interest rate rose from 4.2% to 4.6% (0.4%). This comeback did not surprise us and we think it can be used to accumulate leading sectors and companies with very attractive valuation discounts, especially as we enter the heart of earnings season, which can present us with opportunities.

Equity

Earnings

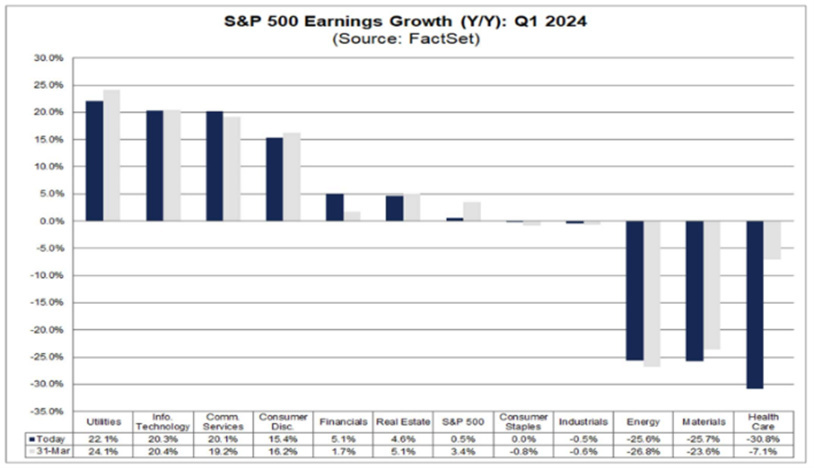

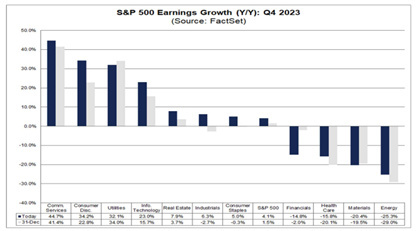

The first-quarter earnings season has just begun with earnings growth of +0.5%, lower than expectations of +3.4% at the end of March. About 14% of companies reported earnings, of which about 74% beat estimates. This earnings season is confirming the last quarter of 2023, i.e. the continued weight of inflation on companies most concentrated in the US. In fact, if we take companies that make more than 50% of their revenue in the US, we see a 3.9% growth in revenue, compared to a modest +2.2% growth recorded by companies that export the most. However, if we look at earnings growth, we see that companies that export the least experienced a -2.5% decline in earnings, compared to those that export which grew 5.9%. We expect this trend to continue and that profits will continue to suffer negative revisions.

Stock Evaluations

The month of April is reminding us of the existence of gravity, which implies that valuations cannot go up indefinitely. The rise in interest rates has corrected valuations by about 5%. We continue to believe that US mid-capitalisation companies, European companies, and in particular Chinese companies, are the ones at the biggest valuation discount.

Equity Sectors

The preferred sectors in the US remain the most defensive: Utilities, Non-Discretionary Consumption and Health Care. Within the Health Care sector we believe that some leading companies in the Health Insurance sub-sector have a very good safety margin.

The preferred sectors in Europe, on the other hand, are: Discretionary Consumption, Non-Discretionary Consumption, Health Care, Real Estate and Industrials.

Bond

On the bond side, we continue to see opportunities in European and US government bonds of long duration. As far as corporate bonds are concerned, we believe that the low level of spreads does not provide investors with the right margin of safety.

Governments

The European Central Bank at its meeting in early April pointed out that the interest rate cut will come at its June meeting. This move is justified by all the macro data, from slowing inflation to lower than expected GDP, which would even justify an immediate rate cut. The ECB did not cut just to avoid a strong appreciation of the dollar that could affect inflation in the future, Europe being a commodity importer. This highlights the strong link between the US and Europe, and how monetary policy decisions between the two central banks will be synchronised.

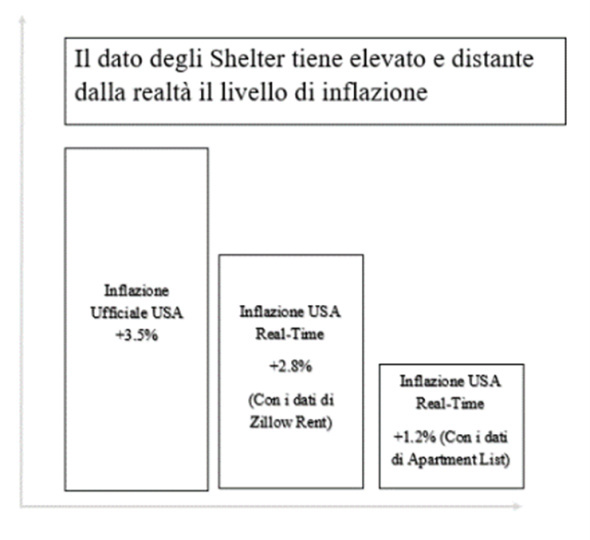

The figure that is leading investors to revise downwards the number of possible Fed cuts is inflation. However, if we adjust the figure considering market data, we get a number that moves between 1.2% and 2.8%, in line with the inflation figure most closely watched by the FED, i.e. the PCE. The point is that inflation is currently affected by the rental component, which is calculated as a consumer survey, not by taking market data.

Corporate

On the corporate bond side, we believe that the current spreads do not allow the investor the correct margin of safety. We start with investment grade corporate bond spreads, which narrowed by 10 basis points to +86. This tightening has brought the spread level to its lowest level in 24 years, only 2% of the time IG spreads have been tighter. We move on to high-yield corporate bond spreads, which narrowed by 10 basis points to 31 basis points at +302. This tightening brought spreads to their lowest level in 24 years, just 3% of the time HY spreads were tighter.

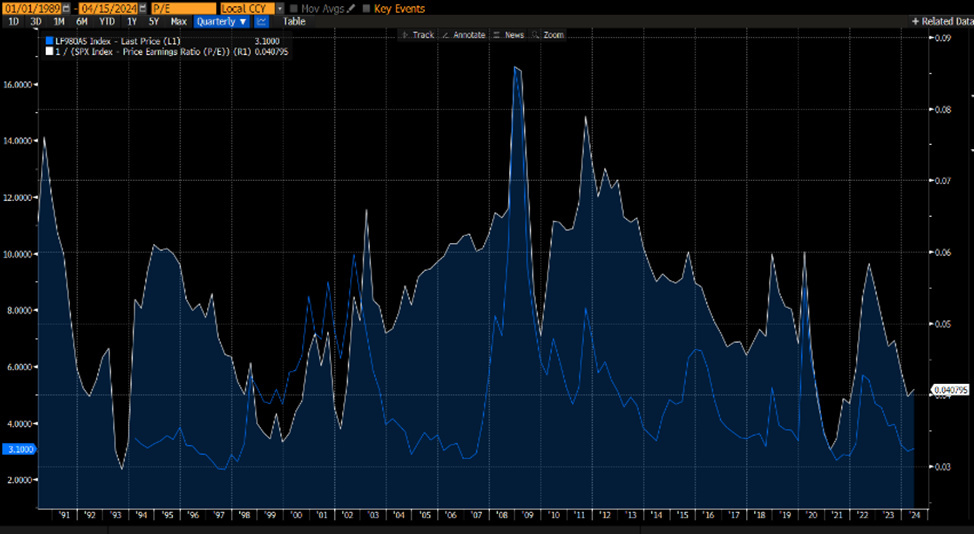

What do these low spreads tell us?

Spreads are the counterpart of valuations in equities. As can be seen from the chart below, bond spreads (blue line) move like equity valuations (white line), valuations expressed as the inverse of the price-to-earnings ratio (the so-called earning yield).

Low spreads on bonds are in fact equivalent to high valuations on equities. Low spreads indicate to us that investors are positive about the asset class and require a lower return to invest in this asset class. However, history teaches us that, as in the case of high equity valuations, low spreads anticipate lower-than-average returns in subsequent years.

Conclusion

In conclusion, we believe that the second quarter started with a return of gravity that brought healthy corrections in equity valuations. The equity market continues to present opportunities and a margin of safety for investors in mid-cap companies, Europe and China. On the bond front, the margin of safety lies in government bonds. Corporate spreads, on the other hand, continue to lack the right valuation profile to balance the risk borne by the investor.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.