When the fundamentals come back to haunt us

16 April 2026 _ News

If we look at what is happening in the markets today, the first thing that stands out is an extremely high level of uncertainty, driven almost entirely by the geopolitical context.

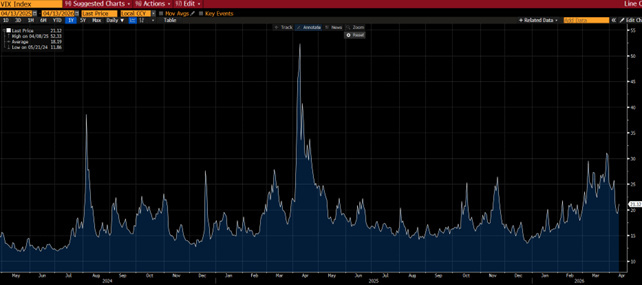

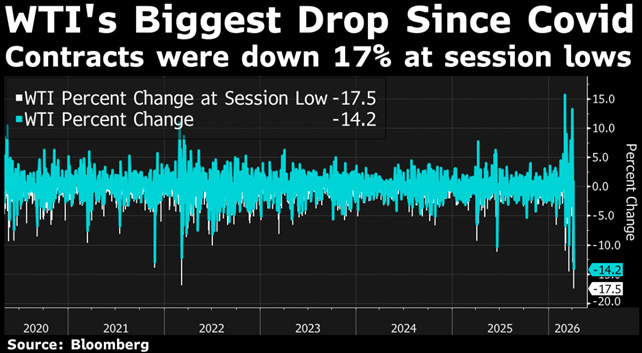

We have seen this clearly in recent days. The announcement of a temporary ceasefire between the United States and Iran triggered a rally, with oil prices falling significantly, bond yields declining, and stock indices posting gains of more than 2–3% in a single trading session, accompanied by a sharp drop in volatility indices.

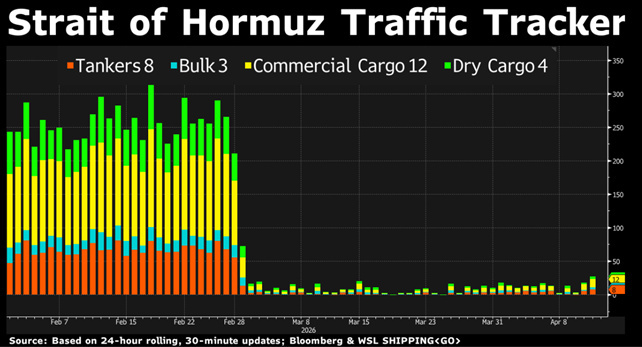

At the same time, however, the market remains extremely sensitive, because this lull is fragile and the situation can change very quickly. In the very short term, the market is not driven by fundamentals, but by a constant repricing of geopolitical risk. And the central issue remains the same: the Strait of Hormuz.

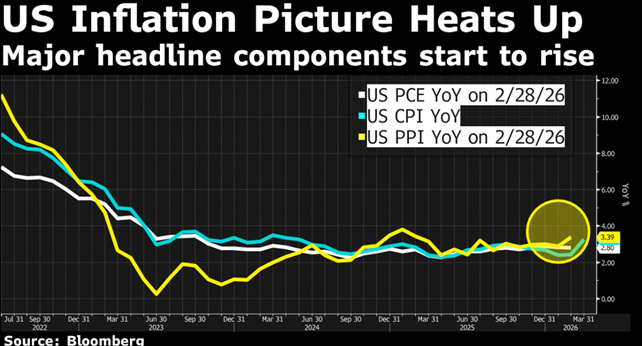

But if we stop here, we risk getting an incomplete picture. Because, on the other hand, the macroeconomic picture isn’t falling apart. Inflation, as reported this week, remains high—around 3% according to the most closely watched measures—but is in line with expectations, even as it continues to be a concern for the Fed.

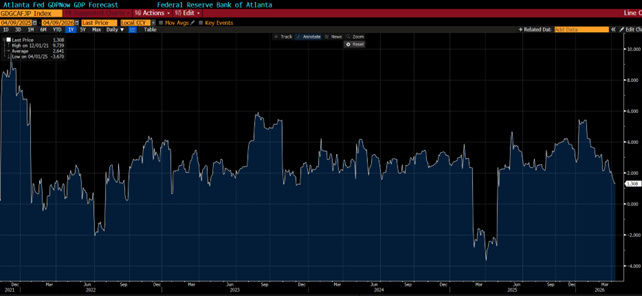

At the same time, however, the labor market is holding up: jobless claims remain at moderate levels and do not indicate significant strain. Consumer spending is slowing, but not collapsing. Economic growth has slowed, but the economy continues to grow.

In other words, the situation is becoming more complicated, but it is not deteriorating in a structural sense, and this is also reflected in the behavior of the markets themselves.

Despite the volatility, we are not seeing a true bear market. Rather, we are seeing a consolidation phase, with sideways movements and very strong shifts beneath the surface. And it is precisely beneath the surface that the most interesting things are happening.

We have seen, for example, how the drop in oil prices immediately benefited certain sectors—such as transportation and airlines—while the energy sector, which had been the big winner during the period of market tension, was the hardest hit.

This leads us to an important point.

The market does not move in a linear fashion. It anticipates, overreacts, and then corrects itself. And this is particularly evident in the case of oil.

Historically, every major spike in oil prices—whether linked to wars, geopolitical shocks, or supply concerns—tends to follow a very specific pattern: a rapid, often sharp rise, followed by a period of normalization in the months that follow. This is because, at the onset of a conflict, markets price in the worst-case scenario; however, in most cases, that scenario does not materialize in its most extreme form. The same applies to energy stocks. In the short term, they benefit from rising oil prices, but in the medium term, they begin to reflect a slowdown in demand, pressure on margins, and a normalization of prices. In other words, the environment is starting to point toward a possible phase of profit-taking in the oil sector.

This is a perfect example of how markets really work: they don’t just react to facts, but to expectations about those facts. And this brings us to another key point: corporate earnings trends and the start of the new U.S. earnings season. Because beyond the geopolitical noise, it will be earnings that bring the market’s focus back to fundamentals.

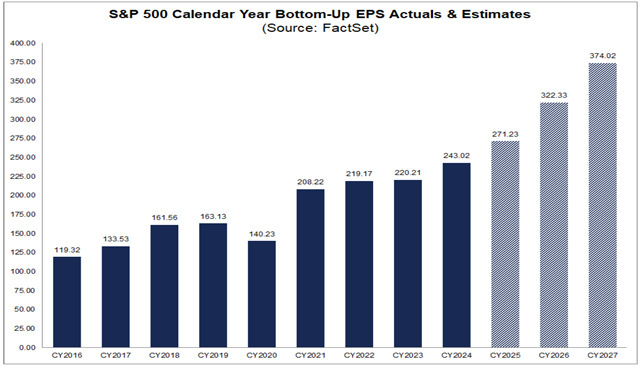

Consensus estimates remain very ambitious at this point. The market expects earnings growth of around 17% for both 2026 and 2027, with a significant contribution from the technology sector and, at this stage, also from the energy and materials sectors. Clearly, these are challenging expectations.

Even when considering the trend in revisions, it is probably easier to envision a downward revision than further upward revisions, especially in a context where macroeconomic and geopolitical uncertainty remains high and energy prices are likely to weigh on consumption and margins.

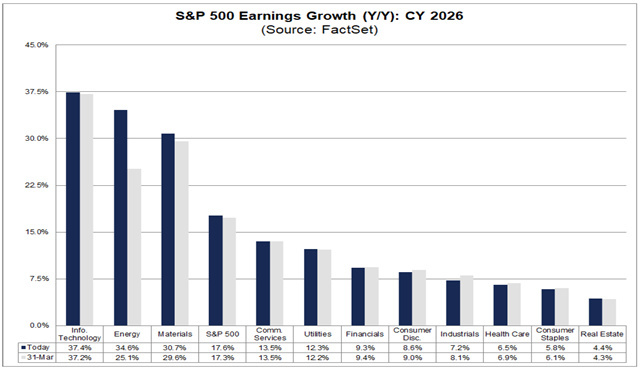

There is another important factor to consider: earnings growth is not uniform. It is largely concentrated in a few sectors, while the rest of the market shows much more moderate growth. Technology, energy, and basic materials are expected to see earnings rise by 30%, compared to industrials, consumer goods, and pharmaceuticals, which are expected to grow between 6% and 8%. This means that the market will likely be more selective and less inclined to reward companies indiscriminately.

That said, there is also a positive factor at play. Compared to the last earnings season, valuations have come down. The repricing we’ve seen in recent weeks has compressed multiples. And this, in very simple terms, means that the market is now paying less for those same growth expectations.

And that's the key point.

When expectations remain high but valuations decline, the market tends to become more receptive to positive surprises. During the last earnings season, both expectations and multiples were very high, making it particularly difficult to elicit a favorable reaction after results were released. Today, however, expectations remain high, but the compression of multiples changes the starting point: an upward revision of estimates is not necessarily required for the stock to react positively. Solid results, coupled with the absence of significant disappointments, may be sufficient.

That said, the overall picture remains balanced. In an environment where expectations are still high, weak guidance or signs of a slowdown—as has already been seen in some cases—are likely to be punished more severely.

So we are now at a stage where earnings season is becoming particularly important.

Because the market is finally refocusing on earnings after weeks in which attention was almost entirely absorbed by geopolitical issues, and in a sense, this is also a positive sign. If earnings once again take center stage, it will mean that geopolitical tensions are gradually receding into the background and that the market can return to focusing on fundamentals.

At that point, with price-to-earnings ratios now at historical averages, the real question will be whether these expectations—which remain very ambitious today—are truly sustainable.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.