AI accounts for 1.2% of US GDP: opportunity or risky concentration?

27 November 2025 _ News

The past week has clearly shown us how quickly market sentiment can change in a matter of hours. We are coming off a difficult November, with the S&P 500 down more than 5% from its highs and the Nasdaq down nearly 8%. Thursday was emblematic: a strong opening, supported by job data and Nvidia's rebound following its quarterly results, quickly turned into widespread losses.

Despite market jitters, the end of the shutdown has brought back something essential for the markets themselves: data.

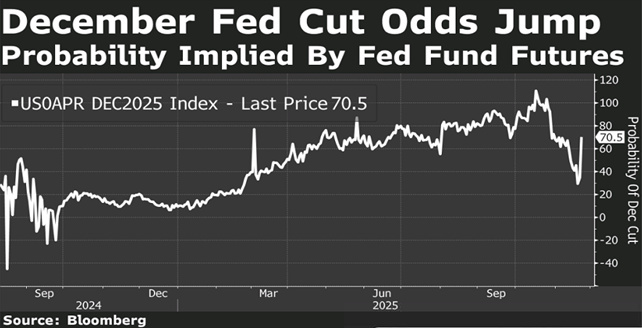

The reopening of the US government has allowed the publication of the September employment report, and the numbers – 119,000 new jobs but unemployment at 4.4% – tell a much more nuanced story than the market expected. It is a sign of a slowdown, but not enough to force the Fed into an immediate cut. In fact, with October and November data due after the FOMC meeting on December 10, the probability of a cut is now around 70%, with the minutes of the previous meeting referring to “strongly divergent views” within the board. It is a context in which monetary policy is sailing without a compass, with the Fed having to make a decision without complete data for the first time in years.

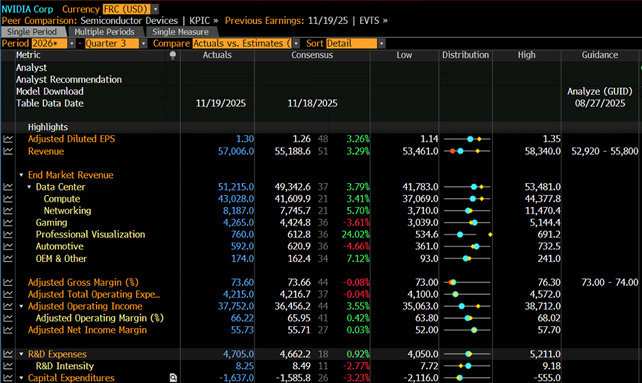

Amid this macroeconomic uncertainty, Nvidia reported an extraordinary quarter—revenue growth of over 60%, rising margins, record backlog—yet the stock closed lower after a brilliant opening.

The stock went from initial euphoria to a sharp decline, losing over 0 billion in market capitalization in just a few hours.

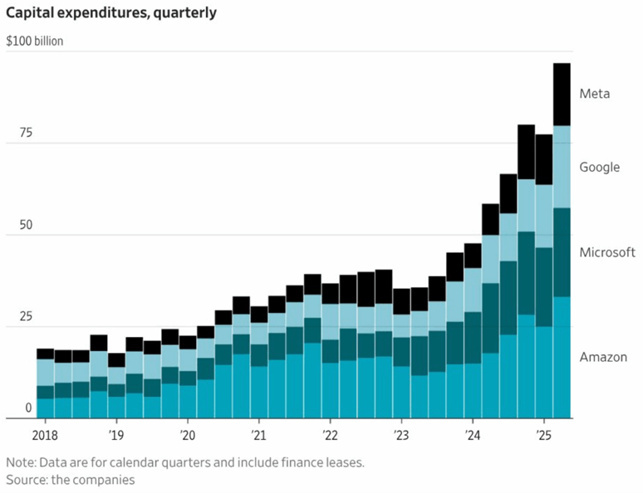

The CEO's reassurances about the “non-AI bubble” did not convince the market, partly due to Ray Dalio's warning that AI is already 80% in a bubble. Analysts' focus has shifted to the “credits” item in Nvidia's balance sheet, which recorded .4 billion in revenue against over billion in data center sales, raising doubts about collection times and the strength of demand. It is a very clear signal: the market no longer rewards growth for its own sake, but wants to understand how sustainable it is. Today's market is no longer satisfied with “how much” AI is growing, but wants to understand “how.” For weeks, doubts have been emerging about the financial sustainability of the data center race. Hyperscalers are financing the AI revolution largely through debt, with issuances we haven't seen in years. The most solid companies—Google, Meta, Microsoft—can afford it; others, such as Oracle, are exposing themselves much more than they should, draining future financial capacity in order not to fall behind.

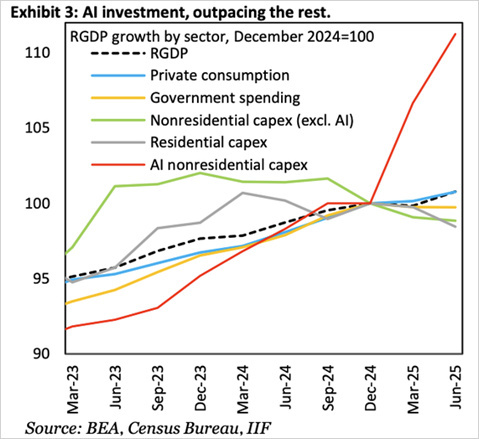

The truth is that a significant part of the apparent resilience of the US economy today does not come from consumption, manufacturing, or real estate. It comes from a single source: capital expenditure on artificial intelligence.

The biggest players in the cloud – Microsoft, Google, Meta, Amazon – are investing at rates never before seen in modern history.

Estimates are constantly being revised upwards: according to various analyses, global spending on AI infrastructure will grow by 67% in 2025 and by another 31% in 2026, reaching over 0 billion. For some of these giants, capex is rising to 30% of annual sales: three times the historical average. These are huge figures, to the point of having a significant macroeconomic impact.

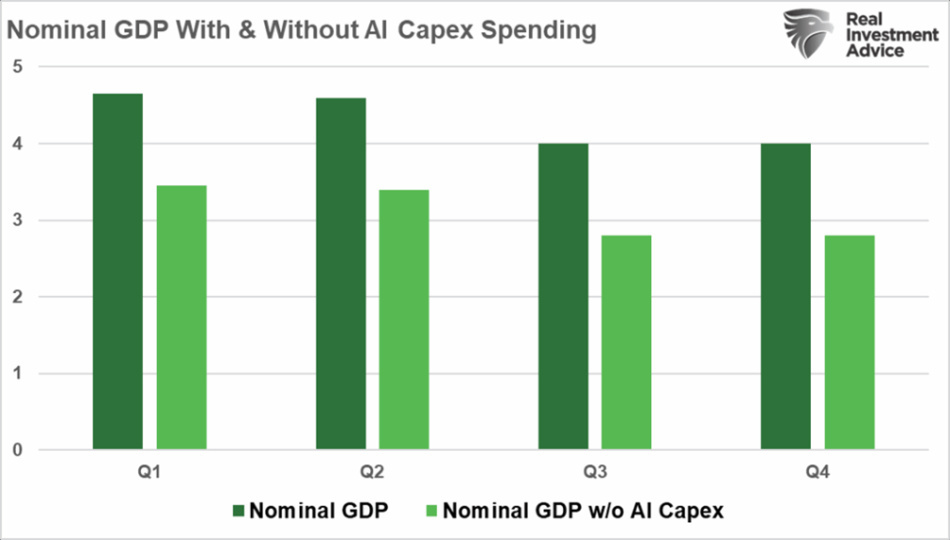

According to the most recent estimates, AI spending in the United States will reach approximately 1.2% of GDP in 2025.

This figure is so large that, if we subtract it, US growth appears much weaker. In other words, the growth we are seeing today is real, but it is not widespread. It is concentrated. And it is concentrated in the hands of four companies.

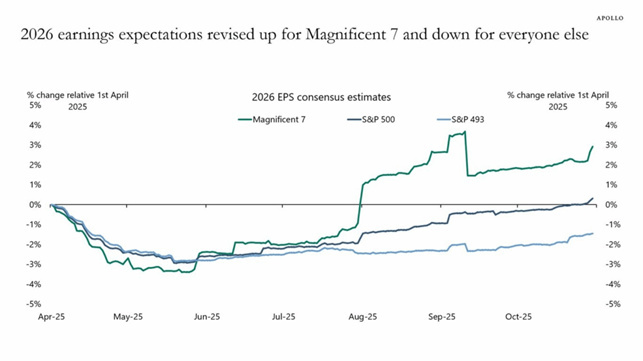

If we look beyond AI, the signs are not as bright: residential investment remains constrained by the inaccessibility of real estate; traditional corporate investment, outside of big tech, is modest; employment is showing signs of fatigue; consumption outside the high-end segment is weak; and many S&P 500 companies—the “493”—are facing stagnant or negative earnings expectations for 2026.

In fact, growth is driven by a hyper-concentration of highly capital-intensive capex, largely based on imported technologies, and therefore with a lower internal multiplier than it appears.

We are far from an investment cycle that spreads throughout the rest of the economy, as happened with infrastructure or the traditional industrial cycle.

Those investing in AI today face an interesting paradox. On the one hand, the opportunity is enormous and concrete: chipmakers, cloud services, hyperscalers, and AI infrastructure could outperform the economy for years to come. The growth trajectory is real. On the other hand, there are significant risks: high concentration of growth sources; economic returns not yet fully proven; very optimistic future earnings; stretched multiples; high potential for disappointment if spending slows.

Just as in 1999, when adding “.com” to a name was enough to raise capital, today many companies are riding the “AI” label without having a sustainable business model.

There will be huge winners. But there will also be many projects that will never see a return.

Today, investors must be selective, disciplined, and aware that not everything that grows in value does so because it creates value.

Nvidia and the Fed, strange as it may seem to say in the same sentence, have something in common today: both depend on data.

The Fed doesn't know how to proceed because the data is missing.

The AI sector is growing at an unprecedented rate because data—and the ability to process it—has become the new currency of economic power. But they also share another element: the fragility of this phase of the cycle. The market today is not saying that AI is a bubble. It is saying that it must become sustainable, widespread, productive. That investing is not enough: real returns are needed, not just ambitions.

It is at times like these that discipline pays off. Understanding where there are genuine opportunities and where growth is artificially inflated by capital expenditure. Where there are real business models and where, instead, the narrative runs faster than execution.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.