Fed, Warsh, and the Risk No One Sees

25 June 2026 _ News

This week, the main focus is the Federal Reserve. On Wednesday, Kevin Warsh held his first press conference as Fed Chair, and what he said — and especially what he did not say — left markets with more questions than answers.

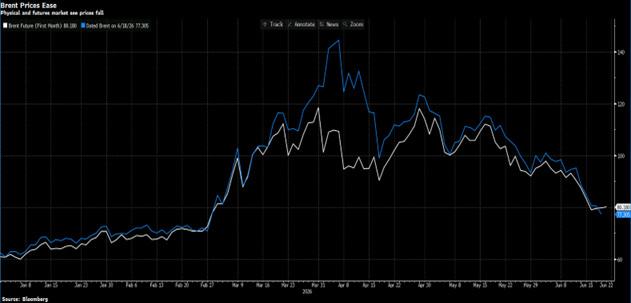

Meanwhile, in the background, the agreement with Iran has officially changed the geopolitical landscape, oil prices have fallen by more than 30% from their recent highs, and U.S. economic data continues to show growth that does not seem to be slowing down.

But let’s start with the Fed, because it is at the center of everything.

As expected, the FOMC left interest rates unchanged. The decision itself did not surprise anyone. What surprised investors was the overall tone of the meeting.

The official statement was the shortest since the Greenspan era — about 130 words compared to more than 300 in April’s statement — and it contained no forward guidance at all. There was no indication of what the Fed might do at upcoming meetings. Warsh explicitly explained that he chose this “say less” approach because he believes it is appropriate for the current environment. However, markets were left wanting more clarity.

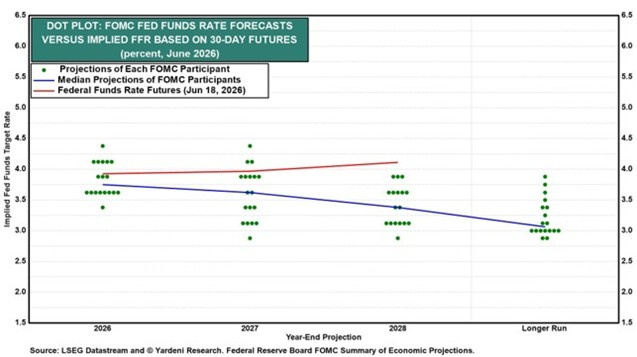

The dot plot — the chart showing individual FOMC members’ interest rate projections — delivered a much clearer and noticeably more hawkish message. The median projection for the federal funds rate at the end of 2026 increased from 3.4% in March to 3.8%. Nine of the eighteen members now expect at least one rate hike this year, while five expect as many as two. In March, twelve of the nineteen members expected at least one rate cut. This is a dramatic shift in just three months.

The Fed’s inflation forecasts explain why. Core PCE inflation was revised upward from 2.7% to 3.3% for this year, and from 2.2% to 2.5% for 2027. The Fed is openly acknowledging that inflation is likely to remain above its target for at least another couple of years.

There is, however, a paradox worth highlighting, because it is counterintuitive. Despite the hawkish shift in the dot plot, U.S. monetary policy is still effectively accommodative.

Why? Because what matters is not the nominal level of interest rates, but the real level — meaning the rate after inflation. With the policy rate at 3.6% and core PCE inflation at 3.5%, the real rate is basically zero. The Fed estimates that the neutral rate — the rate that neither stimulates nor slows the economy — is around 1.1% in real terms. So we are well below that level.

In other words, the language has become tougher, but real rates still support growth. That is not a small detail.

Warsh also announced the creation of five working groups to review the Fed’s communications, balance sheet, reference data, inflation framework, and productivity. It is an ambitious project, but it immediately created a practical problem: markets need to understand how the Fed reacts to data, which variables matter most, and when it is likely to move.

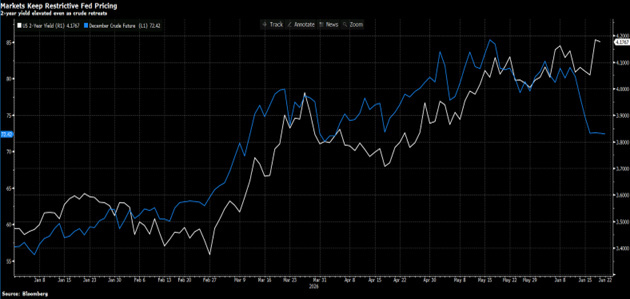

Without forward guidance, and with a Chair who has not yet clearly defined his reaction function, there is a risk that every speech by every FOMC member will be read as an official signal. That could increase volatility instead of reducing it. The two-year Treasury yield, which reflects expectations for short-term rates, rose to 4.20% after the press conference — its highest level of the year.

On the real economy side, however, the picture remains solid. The Atlanta Fed’s GDPNow estimates second-quarter growth at 3.3%. Bank lending continues to expand. The labor market is slowing slightly, but it is not breaking.

Most importantly, with the agreement with Iran signed on Friday in Geneva and oil prices down by more than 30% from their highs, the energy inflation shock — which had been the main driver of rising prices in recent months — is starting to lose strength. If this trend continues, the Fed could find itself in the second half of the year with lower-than-expected inflation and less pressure to act. But for now, this is still only a possibility.

There is one final topic that deserves attention this week. It is less visible, but perhaps more important for anyone managing a medium-term portfolio: the risks quietly building beneath the surface of the market.

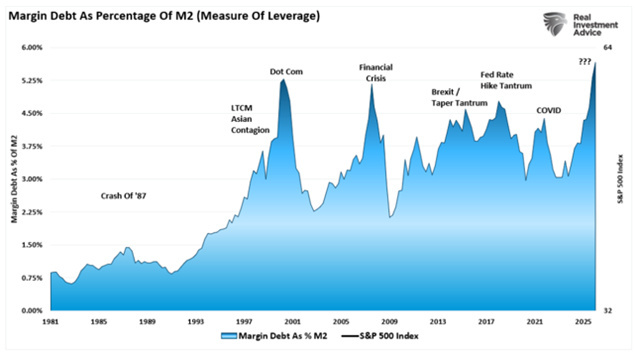

Three stand out in particular. Margin debt — money borrowed to invest — reached .3 trillion in April, an all-time record. That is equal to around 4% of GDP, compared with a historical average of 1.5%. When markets rise with this much leverage, any correction tends to become stronger, because forced selling adds to normal selling.

The second element is the equity risk premium, which is becoming increasingly compressed. The third element is seasonal: historically, the period from May to October has produced average gains for the S&P 500 of just 1.7%, compared with 7% during the winter half of the year. And 2026 is a midterm election year, which has historically been the most volatile phase of the presidential cycle.

None of these three elements, on its own, is a signal of a market reversal. But together, in a context of stretched valuations and a Fed that has just increased uncertainty, they create a risk profile that a careful portfolio manager cannot ignore.

The good news, and this should be said just as clearly, is that the earnings picture remains positive. Analysts continue to revise their estimates upward, the median S&P 500 stock is expected to deliver double-digit growth this year, and historically, periods of strong earnings growth have gone together with better market returns, not worse ones.

There is also an interesting structural argument: profits for the average American company have been broadly flat since 2019, well before the pandemic. The current recovery may therefore not be a phase of overheating, but simply a catch-up after several difficult years. If that is the case, there may still be room for earnings to grow further.

How should investors manage all of this?

Stay invested, but with greater discipline. Do not chase every rally or the next SpaceX-like story. Build cash reserves not to leave the market, but to have ammunition ready when — not if — summer volatility creates opportunities to buy quality assets at better prices.

As Howard Marks once wrote, the most dangerous thing in investing is believing that there is no risk. Today, high-yield credit spreads are near their lows, and the market is pricing in almost no risk at all. This is a time to stay alert.

The long-term trend remains intact. The investor’s job now is to protect what has already been earned, so that they are in a position to participate in what comes next.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.