Market Sell-Off: The Mistake of Waiting for the "Bad News

02 July 2026 _ News

There’s something paradoxical about what happened in the markets this week. During the months when geopolitical tensions in the Middle East kept the world on edge—with oil prices surging and the Strait of Hormuz closed—equity markets continued to climb, driven by enthusiasm for artificial intelligence. Investors sought refuge in technology stocks rather than in traditional safe havens like gold.Then, as geopolitical tensions eased, oil prices fell back to pre-conflict levels and the outlook finally became less uncertain. That was precisely when markets pulled back. The sell-off arrived just as the bad news had faded. Understanding why is well worth the effort.

The spark came from South Korea, where a memory-chip giant whose stock had risen 350% since the start of the year announced a shift in focus toward traditional DRAM — widely used memory chips not designed for AI and far less profitable.For the market, it was a signal: the AI euphoria may be starting to slow. The Seoul stock market lost 10% in a single session, dragging Wall Street down with it. From Nvidia to Micron, the semiconductor sector suffered a sharp sell-off. The move has been described as profit-taking after months of stellar gains, compounded by a more restrictive-than-expected Fed under Warsh and the growing realization that the debt accumulated to fund AI investments will have to contend with higher interest rates. Not everyone reads the situation so gloomily — and Micron, which reported results above expectations, helped stabilize sentiment toward the end of the week. But the signal from South Korea left its mark. There is also another episode worth paying attention to, because it says something not so much about SpaceX itself — which has since almost returned to its IPO price — but about the broader state of the markets. Just days after its record IPO, SpaceX returned to the market with a billion bond issuance.

A company that had just raised more than billion through its listing, and that is still operating at a loss in two of its three business segments, returning immediately to the market to ask for debt is not exactly a great sign. And the fact that SpaceX had to offer a higher yield than companies with a similar credit rating suggests that bond investors — generally more detached than equity investors — are assessing the risk very differently. Credit spreads are at historic lows, while equity valuations are at historic highs: exactly the kind of environment in which companies have every incentive to raise capital before conditions change. And when companies themselves seem eager to protect themselves, it is fair to start asking questions.

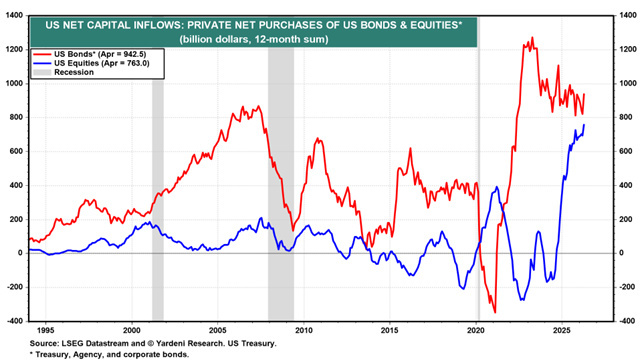

On the macro front, this week saw the release of May PCE data — the inflation measure most closely watched by the Fed. The headline index rose 4.1% year over year, while core PCE came in at 3.4%. With oil prices falling rapidly, June’s headline figure should decline meaningfully. The problem, however, is that core inflation — the measure of underlying price pressures, excluding energy — has remained above 3% for more than five years. That is not a problem that can be solved simply by lower crude prices. Meanwhile, the real economy continues to surprise: May retail sales rose 0.9%, twice expectations; the labor market remains resilient; and first-quarter GDP was revised up to 2.1%. Foreign investors, meanwhile, are not selling America. Foreign capital flows into U.S. equities reached 4 billion over the past twelve months — an all-time record

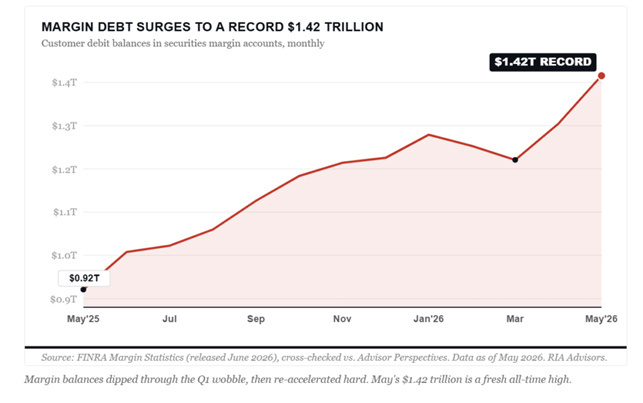

But it is precisely when everything seems to be going well that it makes sense to stop and ask a few uncomfortable questions. Margin debt — the money investors borrow to buy stocks — reached .42 trillion in May, rising 8.5% in a single month and 53.7% year over year. To find a similar expansion, one has to go back to 2021 and 2000. Net debt relative to available cash has reached a record negative level of nearly trillion: investors have almost no liquidity cushion left behind them. This is not a signal that the market is about to reverse. It is something more subtle: the fuse. When conditions turn, brokers force sales, margin calls pile up, and forced liquidation triggers further liquidation. There is no advance warning..

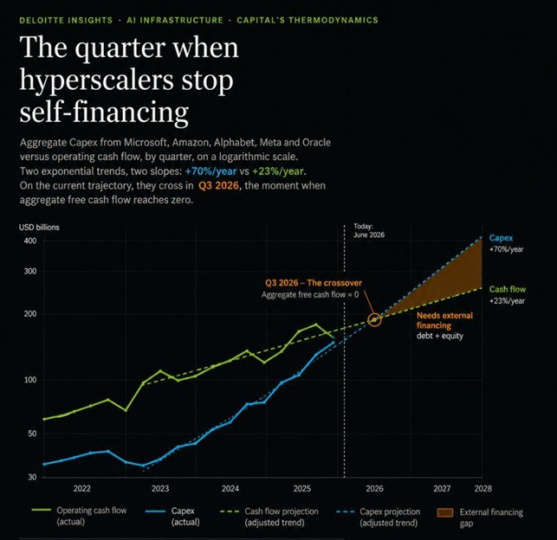

Added to this is a less discussed but highly relevant medium-term issue: the way large hyperscalers account for their spending. Meta, Microsoft, Alphabet, Amazon and Oracle are investing enormous sums in AI infrastructure — 2 billion in 2025, with estimates rising to 0 billion in 2026. But these expenditures are capitalized and amortized over time, rather than fully recognized in the income statement in the year they are incurred. The result is that revenues are growing today, while expenses appear compressed. The gap between actual spending and recorded depreciation in 2026 is estimated at around 9 billion — money already spent but not yet reflected in earnings. When it does appear, hyperscaler margins will come under significant pressure. The question is not whether this will happen, but whether revenues will grow fast enough to offset it.

Finally, there is a theme that is likely to return forcefully in the coming weeks: European defence. Germany has cancelled the €10 billion contract for the F126 frigates, after costs rose to €18 billion and delays accumulated, hitting Rheinmetall’s share price hard. This is not just an industrial story. It is a signal that investor enthusiasm for the sector — driven by rising military spending and the narrative of strategic autonomy — is now colliding with the reality of public procurement, execution delays and sudden political reversals. Defence remains structurally interesting, but here too the gap between the long-term trend and the price already paid for that trend has become a decisive variable.

In short, this week’s paradox tells us something important. Markets do not always react to news in the way one might expect. They rise when they “should” fall, and fall when the news improves. What ultimately matters is the underlying structure: valuations, leverage, confidence and expectations. The technology sell-off is not necessarily the end of the cycle — earnings remain real, and the trend is still intact. But the structural signals now accumulating point to a market environment in which complacency is the main risk. Stay invested, yes. But with eyes wide open — and without forgetting that risks exist even when the headlines are talking about something else.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.