Q2 Earnings Season: The Question Isn't "How Much Will Earnings Grow?"—It's "Will It Be Enough?"

16 July 2026 _ News

This week, something happened that, on paper, should have unsettled the markets: the ceasefire between the United States and Iran collapsed. After Iranian attacks on several ships passing through the Strait of Hormuz, the Trump administration declared the truce over, while the U.S. Treasury revoked the licence that had authorised the sale of Iranian oil. Oil climbed back above , Treasury yields rose again — with the 10-year yield reaching 4.57%, its highest level in more than a month — and equity futures opened lower. And yet, looking at the market as a whole, what happened was not what many would have expected. There was no panic. Instead, there was a rotation. That is the key takeaway from the week: a market that is not falling, but changing its shape.

Let's start with the most visible development—one that received far less attention than it deserved in the headlines. Beneath the surface of major indices still hovering near their highs, the technology sector is undergoing a genuine correction. Around 80% of technology stocks are now in correction territory—down at least 10% from their recent highs—while roughly 60% have entered a bear market, having fallen more than 20%. The latest catalyst came from Samsung. The company released preliminary results showing operating profit had increased nineteenfold, driven by AI demand, reaching billion. Yet the stock still declined, because investors' expectations had risen even faster than its earnings.

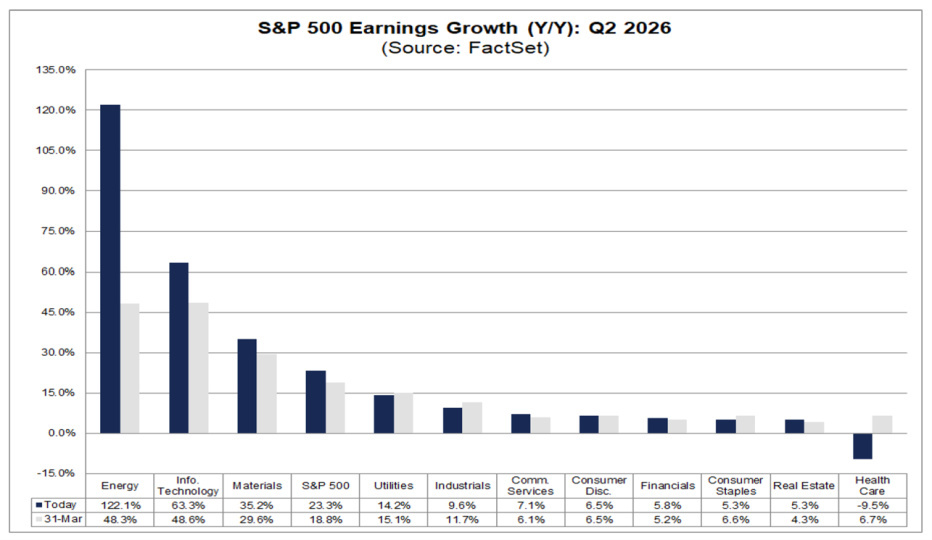

It's the same script we've seen play out for weeks: when a stock is priced for perfection, even extraordinary results may not be enough. And with the second-quarter earnings season kicking off this week, that script could be repeated many times. This brings us to the central point: expectations for this earnings season are exceptionally high. Analysts are forecasting S&P 500 earnings growth of 23% year over year for the second quarter, led by a 120% surge in the energy sector and a 65% increase in technology.

These are numbers that leave very little room for error, especially for the hyperscalers and the biggest AI names, where investor positioning remains crowded despite the recent wave of profit-taking.

The real risk is not that earnings will disappoint—they almost certainly won't—but that they will fail to exceed expectations that have become increasingly unrealistic. The key question for this earnings season is no longer, "How much will earnings grow?" but rather, "Will it be enough?"

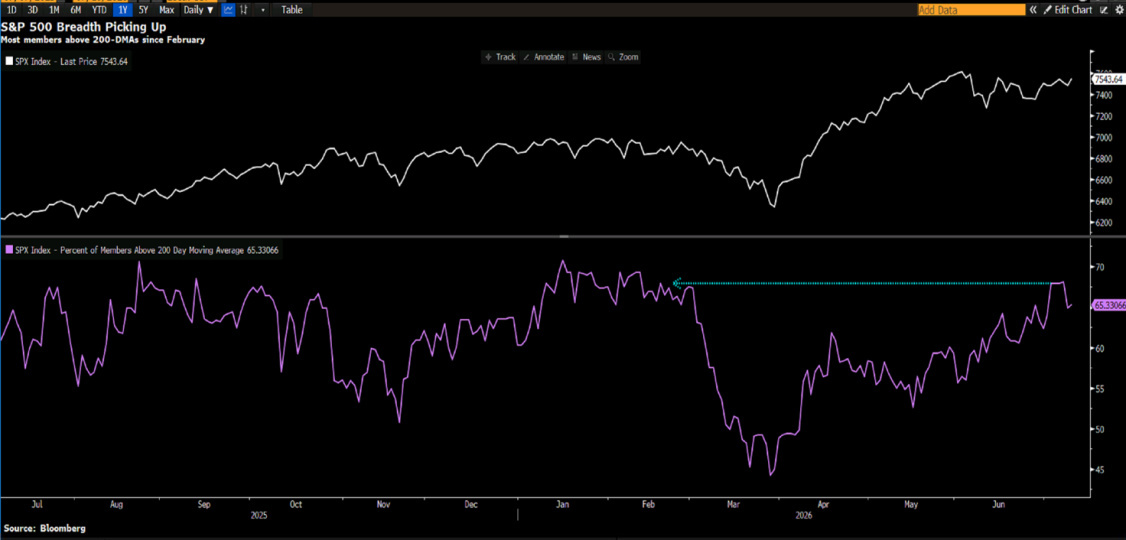

And this is where the week's most interesting development emerges: the market seems to have already started answering that question, and the answer is rotation. While the market-cap-weighted index has been stuck around 7,500 for weeks, the equal-weight index—where each of the 500 companies carries the same weight—has been making new all-time highs. The Russell 2000 small-cap index has joined the move. The Value index is breaking out into record territory, while Growth has stalled. In other words, capital is not leaving the market—it is rotating away from the winners of the past eighteen months and toward the sectors that have been left behind. This is both a sign of a maturing cycle and a sign of market health: a broadening market is structurally more resilient than one driven by just a handful of stocks.

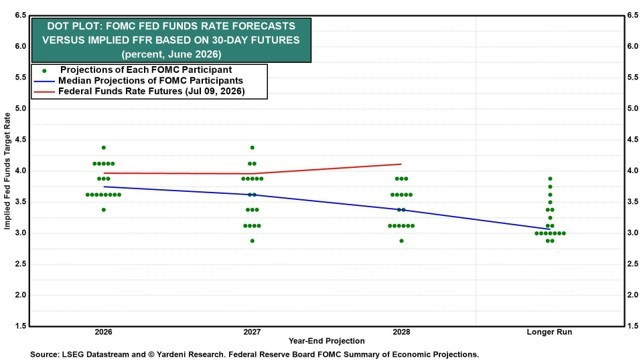

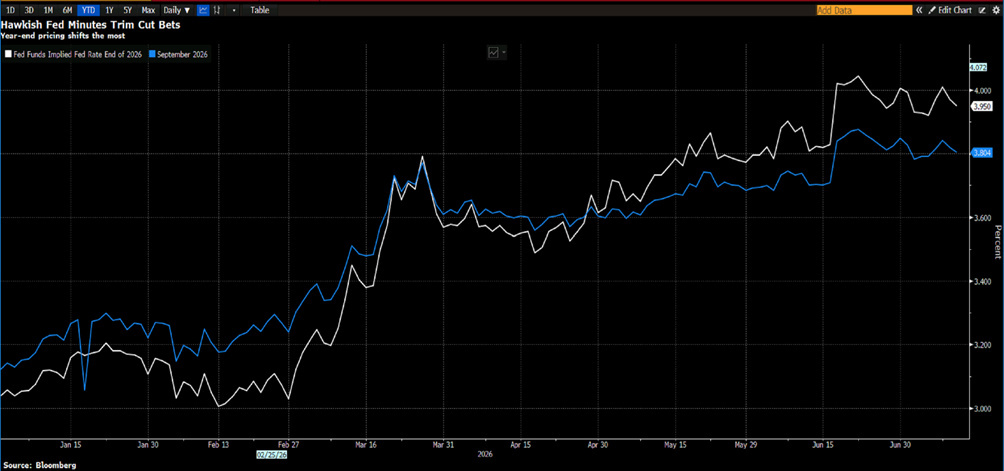

On the Federal Reserve front, the minutes from the June meeting, released this week, confirmed in black and white just how serious the hawkish shift has become. The discussion has moved from when to begin easing monetary policy to whether further tightening may still be necessary. Several policymakers explicitly argued in favor of a rate hike as early as the June meeting.

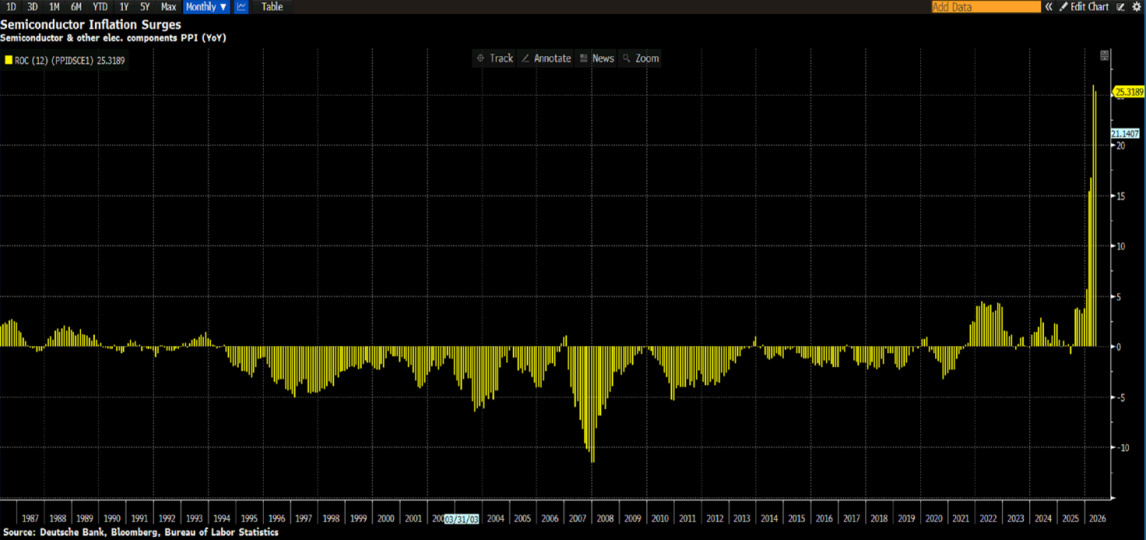

The most significant takeaway concerns the Fed's assessment of the labor market. Downside risks to employment have eased, giving policymakers greater scope to focus almost exclusively on inflation. And inflation remains the central concern. Headline PCE stands at 4.1%, with core PCE at 3.4%. The minutes describe price pressures as becoming "increasingly broad-based"—no longer driven solely by energy, but also by tariffs, AI-related demand, and ongoing supply chain disruptions. One particularly noteworthy detail: artificial intelligence was mentioned 21 times in the minutes, up from just eight in April, and almost always in an inflationary context. The Fed is effectively acknowledging that AI is boosting economic growth and supporting employment, but is also putting upward pressure on prices—particularly for technology and electricity, at least in the short term—and may even be pushing up the economy's neutral interest rate.

Fed funds futures are now pricing in a greater than 75% probability of at least one rate hike before year-end. The renewed tensions with Iran, which have pushed oil prices higher once again, only reinforce that outlook.

Meanwhile, the real economy continues to send mixed but, overall, solid signals. The Atlanta Fed’s GDPNow model estimates second-quarter growth at just 1.4%, but the figure is being distorted by imports. The United States is importing record volumes of AI-related technology from Taiwan, South Korea, and Vietnam, and imports are mechanically subtracted from GDP in the national accounts.

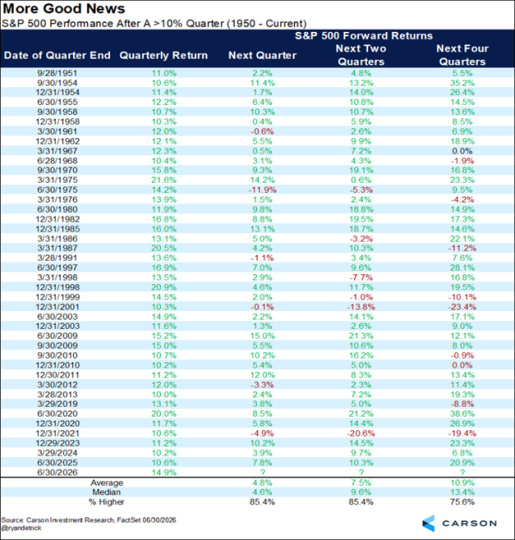

Looking beneath the surface, final sales to private domestic purchasers—the cleanest measure of underlying domestic demand—are growing at 2.9%, up from 1.7% in the first quarter. Consumer spending has rebounded to 2%, while business fixed investment is expanding at an 8.2% annualized pace. Weekly retail sales are up 10% year over year, the strongest growth rate since 2022. This is not an economy that is breaking down. It is an economy growing strongly enough to keep the Federal Reserve on alert. Before turning to the practical takeaway, it is worth remembering the other side of the coin, because the outlook is not defined by risks alone. The first half of the year ended with the S&P 500 up 9.6%, while the second quarter—with a gain of nearly 15%—was the strongest second quarter of a U.S. midterm election year since 1950.

Historical statistics should be viewed for what they are: probabilities, not promises. Even so, they provide more than one reason for optimism. Whenever the S&P 500 has delivered a double-digit gain in a single quarter, it has gone on to rise over the following two quarters in more than 85% of cases.

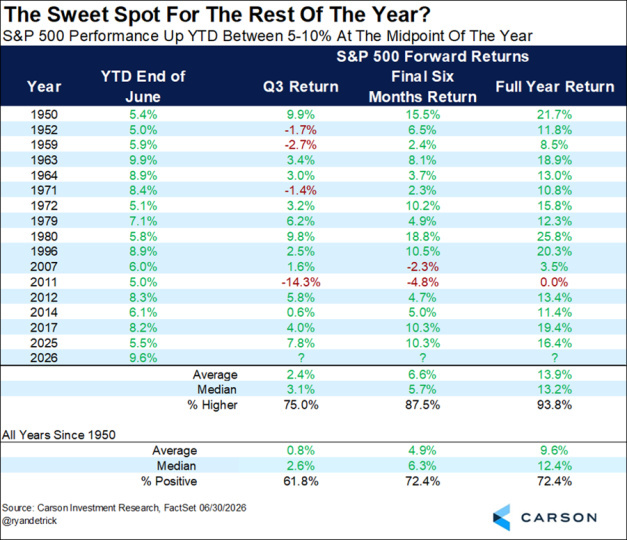

When the first half of the year ends with a gain of between 5% and 10%—roughly where we are today—the second half has been positive in nearly 88% of historical cases.

Historically, July has also been one of the strongest months of the year. None of these statistics guarantees anything, but taken together they suggest that, as long as the underlying trend remains intact, momentum is still on the market's side. That is why the key message is not "get out of the market," but "stay invested with discipline."

So what is the practical takeaway?

First, the ongoing rotation should be viewed as an opportunity rather than a threat. Investors with portfolios heavily concentrated in AI winners have a window to rebalance toward the sectors now attracting fresh capital—healthcare, financials, and high-quality industrials—without being forced to sell into panic.

Second, the earnings season that begins this week is likely to bring significant stock-specific volatility, with companies that miss expectations—even by a small margin—potentially facing sharp sell-offs. It is far better to enter this period with position sizes already aligned to your risk tolerance than to be forced into adjustments while markets are open.

Third, the return of geopolitical risk is a reminder not to abandon cash altogether. In a market where leverage remains near record highs and investors' cash allocations are close to historic lows, having liquidity available to deploy when others are forced to sell is not simply an exercise in prudence—it is a competitive advantage.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.