S&P500 earnings: half of the growth is purely accounting-driven

09 July 2026 _ News

If we had to choose just one metric to assess the overall health of the equity market, we would choose corporate earnings. Without hesitation, because they are the most reliable compass investors have.

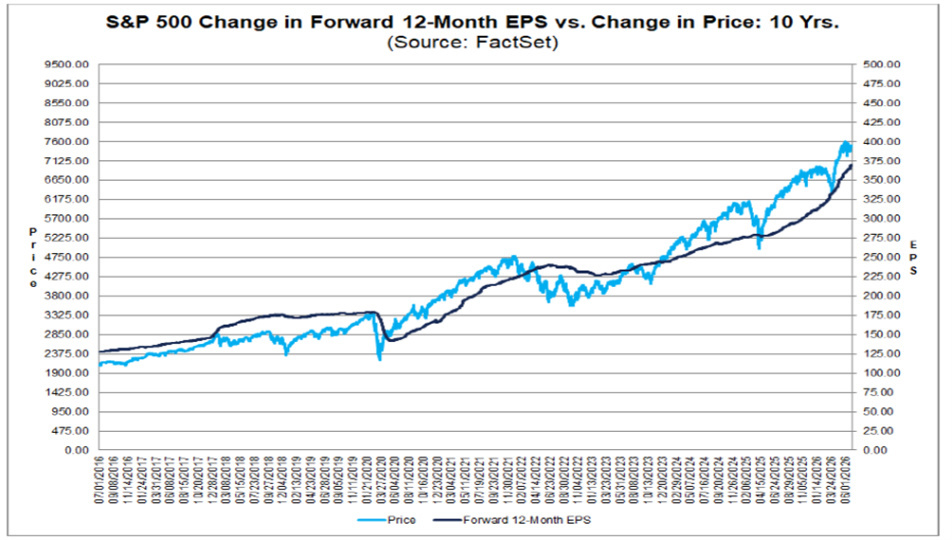

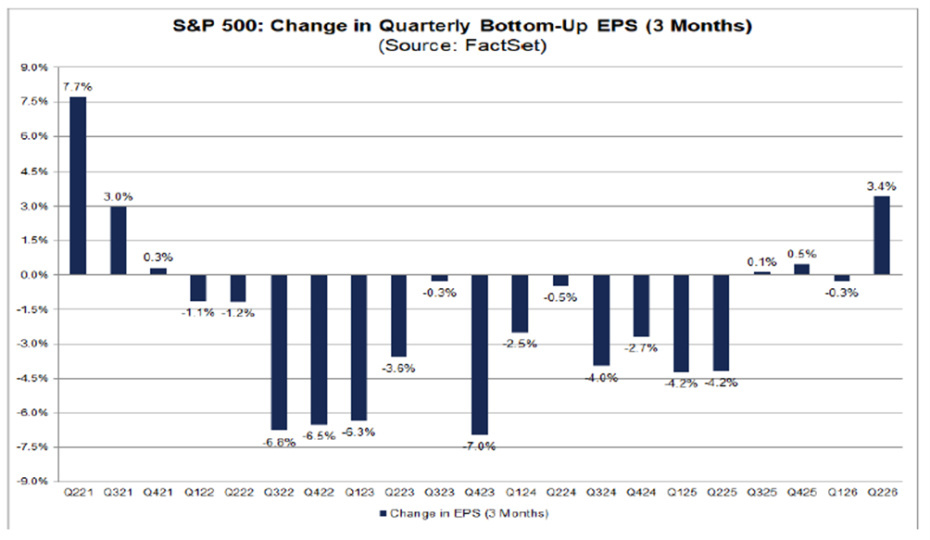

And precisely because it is so important, we cannot avoid highlighting and explaining the extraordinary nature of the current earnings cycle, starting with a figure that shows just how unusual this moment is: analysts raised their S&P 500 earnings-per-share forecasts by 3.4% over the course of the quarter.

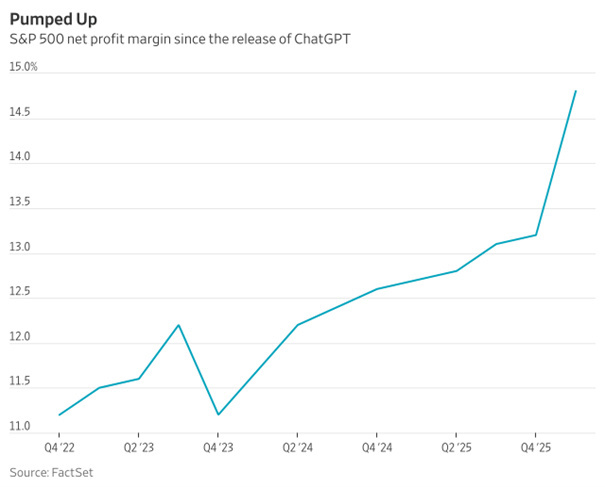

It may seem like a technical detail, but it is not. Analysts usually do the exact opposite: they lower estimates during the quarter, by an average of 2.7%, allowing companies to “surprise” to the upside when they report results. It is a well-established Wall Street ritual. This time, that ritual has been reversed: estimates went up, not down. And there is another exceptionally rare figure: the margin recorded in the first quarter, at 14.8%, is roughly twice the post-war average.

Estimates for the second quarter point to earnings growth of more than 20% year on year. Under normal conditions, these are numbers usually seen during a recovery from recession, not in the sixth year of an expansion.

A closer look at the figures shows that a substantial part of first-quarter earnings growth — around 12% of total S&P 500 earnings — did not come from the sale of products or services. It came from an accounting rule.

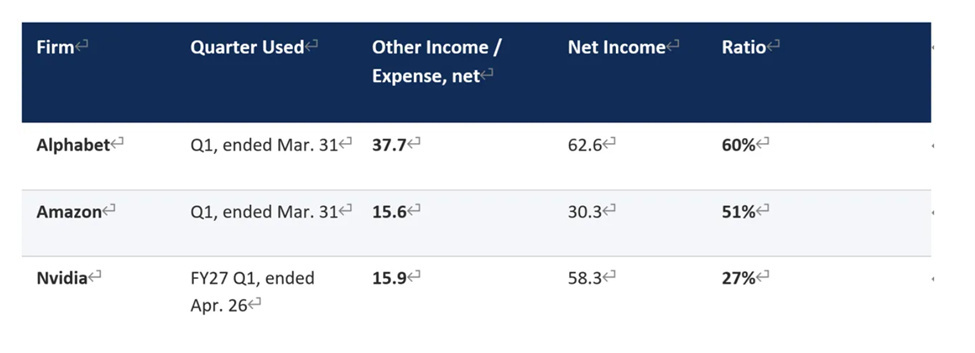

Alphabet, Amazon and Nvidia hold stakes in unlisted AI companies such as Anthropic and OpenAI. When these companies raise capital at higher valuations, listed companies are legally required to revalue those stakes and record the gain in their income statement — even if the gain is purely on paper, not realized and not operational.

In the first quarter alone, this mechanism generated 69 billion dollars in “virtual” earnings for just three companies. In that quarter, 60% of Alphabet’s net income, 51% of Amazon’s and 27% of Nvidia’s came from this accounting item.

Why does this matter? Because first-quarter S&P 500 earnings grew by 28–29% year over year—a figure that excited analysts and helped justify elevated market valuations. But if those 69 billion dollars of accounting gains are excluded, earnings growth falls to around 16%, almost perfectly in line with the historical average of the past five years. In other words, nearly half of the extraordinary growth celebrated by the market did not reflect an improvement in companies' underlying operating performance. Instead, it reflected the fact that private AI startups continued to raise capital at ever-higher valuations.

Even more striking, preliminary estimates suggest that the accounting impact in the second quarter could be two to three times larger. This means that when the trend eventually reverses—and sooner or later it will—the market could face an equally sharp adjustment in the opposite direction.

This matters for two reasons. First, these earnings are not necessarily repeatable. They are not generated by operating activity, and if private company valuations were to decline—even because of a less favorable funding round—the same accounting rules would produce equally significant paper losses. Second, a more subtle dynamic is emerging: a self-reinforcing feedback loop. Public markets rally on the AI narrative, supporting ever-higher valuations for private AI companies. Those higher valuations create accounting gains for listed companies, which in turn fuel even greater optimism in public markets. The cycle feeds on itself until it eventually breaks.

This does not mean that operating fundamentals are weak. Amazon Web Services and Google Cloud, for example, continue to deliver excellent growth. But it is essential to distinguish between genuine business growth and accounting-driven gains. Without these revaluations, first-quarter earnings growth would have been around 16%, broadly in line with the historical average—not 28%.

On the macroeconomic front, the week delivered mixed signals. The U.S. labor market surprised to the downside: the Bureau of Labor Statistics reported just 57,000 new jobs in June, well below expectations of 115,000. The ADP private employment report had already pointed to a softer picture, with 98,000 new jobs. Job openings fell to their lowest level in two years. Meanwhile, the unemployment rate remained at 4.2%, while wages increased by 3.5% year over year—below the inflation rate, meaning workers' real purchasing power continues to erode. This is not a labor market in crisis, but the cooling trend is becoming increasingly evident. Companies are hiring more cautiously, while workers are becoming more reluctant to change jobs amid growing uncertainty.

Manufacturing, however, is holding up: the ISM Manufacturing PMI came in at 53.5, close to its highest level in four years, supported by AI, defense spending and inventories built up during the Gulf crisis.

On the Federal Reserve front, Kevin Warsh spoke this week in Sintra, Portugal, and clearly reaffirmed the stance he had taken at his first press conference: no forward guidance, an absolute commitment to price stability, and a non-negotiable 2% inflation target.

The interesting new element is that Warsh said he was pleased to see bond markets responding positively to his approach: ten-year breakeven rates — which measure expected inflation — fell to 2.30%, signaling that the market believes in the Fed’s seriousness when it comes to controlling inflation.

This is not a trivial signal. Warsh is essentially saying that he prefers to be guided by bond markets rather than guide them through explicit statements. It is a coherent philosophy, but one that leaves a great deal of uncertainty around every meeting.

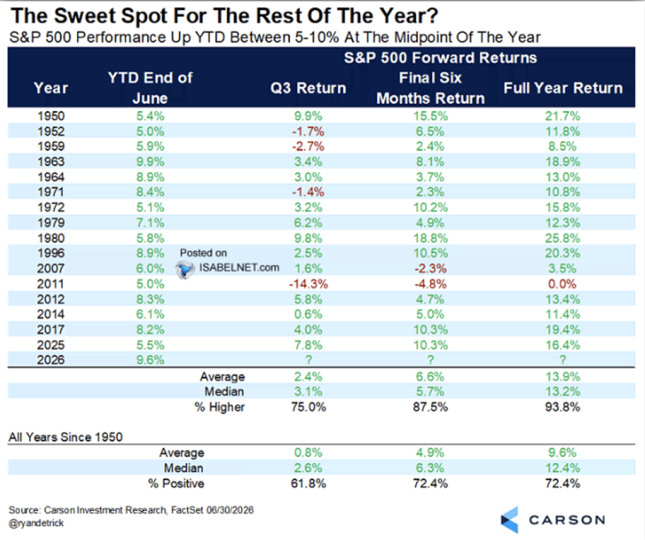

Finally, seasonal statistics deserve an operational mention. The S&P 500 ended the first half of the year up around 9.5%. Historically, when the market rises between 5% and 10% in the first half of the year, the second half closes higher in 87.5% of cases, with an average gain of 6.6%. The odds are favorable.

But the third quarter — July, August and September — has historically been the weakest of the year, with an average gain of just 2.4%. And 2026 is a midterm election year, traditionally the most volatile year of the four-year presidential cycle.

What should investors do with all of this? Stay invested, because the long-term odds remain favorable and underlying operating earnings, after stripping out accounting distortions, are still solid. But do so with greater discipline and less complacency than current market sentiment might suggest.

In summary, the second quarter is ending with numbers that appear extraordinary, but they deserve a closer look. Genuine operating growth is there, but a meaningful share of reported earnings is accounting-driven and should not be expected to repeat automatically. The labor market is cooling, while the Federal Reserve remains on hold. The broader trend remains intact, and history suggests the second half of the year is generally supportive. But the path between July and October is rarely as smooth as the long-term averages imply.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.