Stocks and bonds are telling two different stories

28 May 2026 _ News

Over the past few weeks, we’ve talked a lot about the strength of the market, corporate earnings, the resilience of the US economy, and the fact that, despite a complex macro and geopolitical backdrop, equities have remained surprisingly strong. Today, however, I’d like to slightly shift the perspective, because this week the most important message is not coming only from equities, but above all from the bond market.

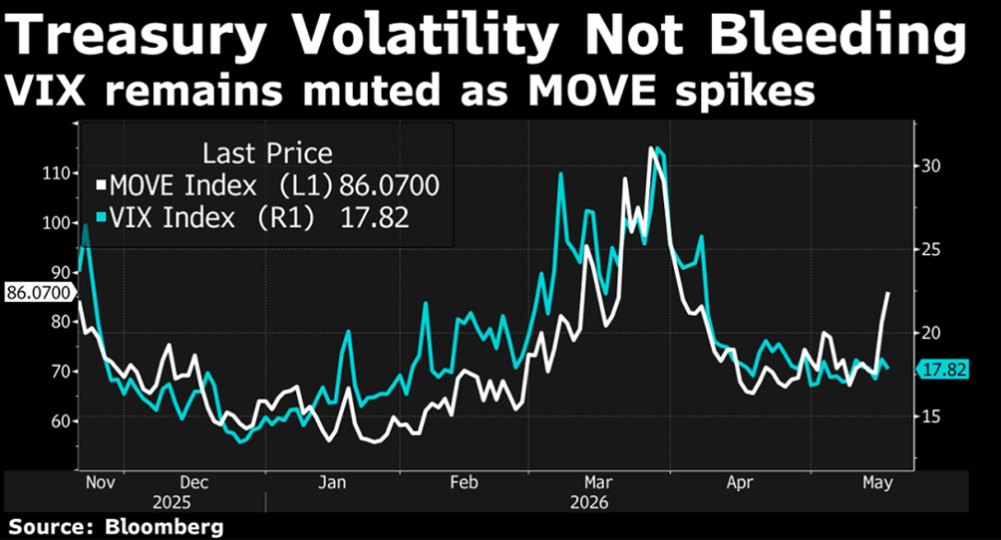

While US indices remain close to their highs, earnings continue to surprise to the upside, the reporting season closed with overall spectacular numbers, and the artificial intelligence theme continues to support a significant part of the market, Treasury yields have also moved sharply higher, approaching levels that many investors consider a sort of “pain threshold” for financial markets.

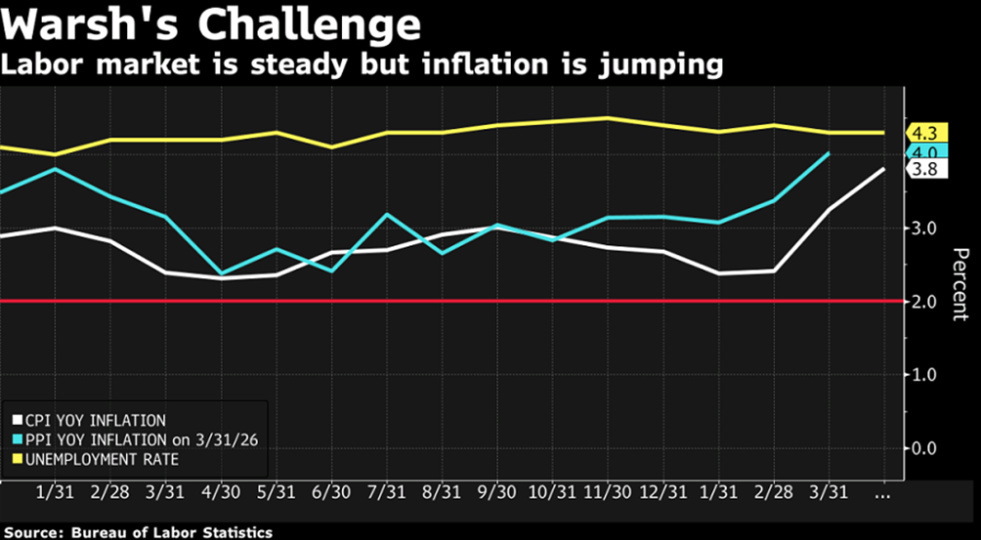

And it is precisely from there that the clearest message is emerging, directed both at the Fed and at US policymakers: inflation is no longer just background noise that can be ignored, but a variable that the bond market is once again pricing with much greater severity. And that is exactly the central tension shaping these past few days.

On one side, the equity market is focused on earnings, nominal growth, the resilience of the US economy, and major structural investments, starting with AI.

On the other side, the bond market is looking at oil above 0 a barrel, the Strait of Hormuz still blocked, elevated deficits, less certain foreign demand for Treasuries, and a Federal Reserve that risks remaining too accommodative relative to persistent inflation.

In other words, stocks and bonds are reading the same scenario through two different time horizons. Equities continue to say: as long as earnings keep rising, the cycle remains intact.

The bond market, instead, is saying: be careful, because if inflation stays high, someone will eventually have to pay the price. The move in yields has been significant.

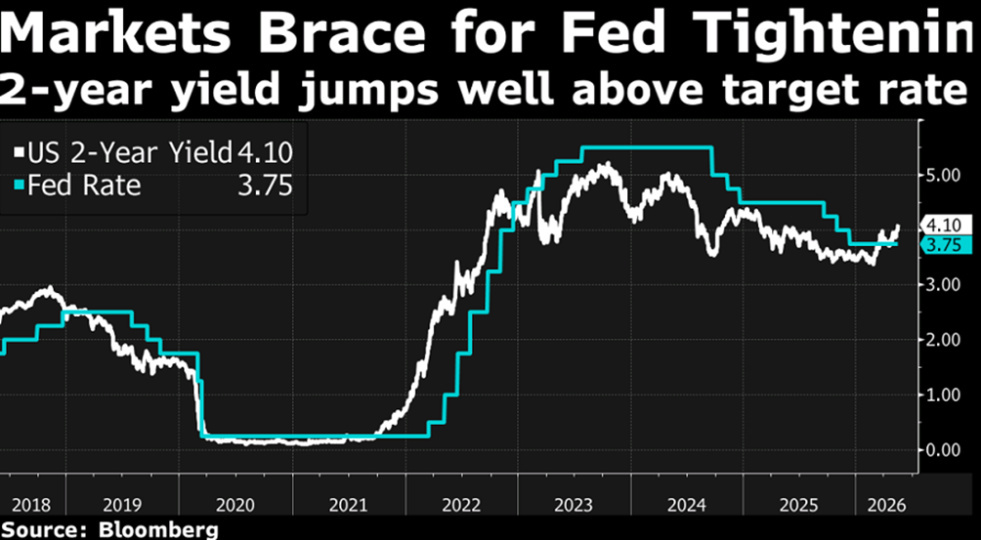

Since the beginning of the Middle East crisis, the 2-year Treasury yield has risen by around 75 basis points, the 10-year by more than 70 basis points, while the 30-year yield has moved back above 5%. The message is clear: markets are no longer positioning for a Federal Reserve ready to cut rates, but are even starting to price in the possibility that the next move — if inflation does not ease — could be in the opposite direction.

The Fed minutes revealed a committee far more divided — and far more concerned about inflation — than the market may have wanted to believe. Several members were already in favor of removing the accommodative bias, and the discussion is no longer just about how long rates should remain on hold, but rather what should happen if inflation stays above target for longer than expected.

And in this environment, the bond market is playing its classic role: it is applying pressure. The so-called bond vigilantes are effectively telling the Fed that if inflation does not come down and oil prices remain elevated, the risk is no longer just slowing the economy too much. The real risk is losing credibility on price stability.

Higher rates do not necessarily end a bull market, but they do change the standard by which markets are evaluated. One of the most anticipated events of the week was undoubtedly Nvidia’s earnings report, because today Nvidia is no longer just a company: it has become the most important barometer of the investment cycle tied to artificial intelligence.

Once again, the numbers were impressive: record revenues, extremely strong growth in the data center segment, high margins, and guidance above expectations. We are talking about growth rates in the range of 80–90%, results that, taken individually, would be extraordinary for almost any company.

And yet, the stock reaction was not particularly enthusiastic. And that is precisely the interesting point. The market was not questioning whether Nvidia would deliver strong numbers; the issue is that expectations had already become extraordinarily ambitious. At this stage, it is no longer enough to confirm that demand is huge — companies must surprise a market that has already priced in a great deal of optimism. This applies to Nvidia, but increasingly to the broader market as well. We have returned to a phase similar to the beginning of the year, where fundamentals remain solid, but the price investors are willing to pay for those fundamentals has become far more demanding.

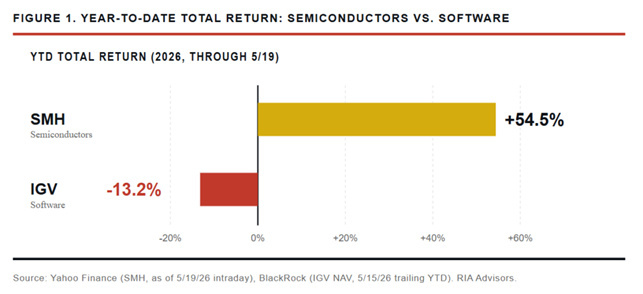

And here we can briefly touch on the theme of internal rotation within the technology sector. In recent months, the market has rewarded the hardware side of artificial intelligence in an extraordinary way: semiconductors, memory, and infrastructure. Software, by contrast, has lagged significantly behind, weighed down by concerns that AI could compress margins and reduce pricing power across certain business models.

But the divergence has now become extreme. And when a divergence becomes extreme, sooner or later the market starts to question whether it may have overdone things in both directions: too much enthusiasm for one part of the value chain, too much pessimism for the other.

That does not mean indiscriminately buying software stocks or selling semiconductors. It simply means that the easiest phase of the AI rotation may now be behind us, and portfolios therefore need to be rebalanced more carefully.

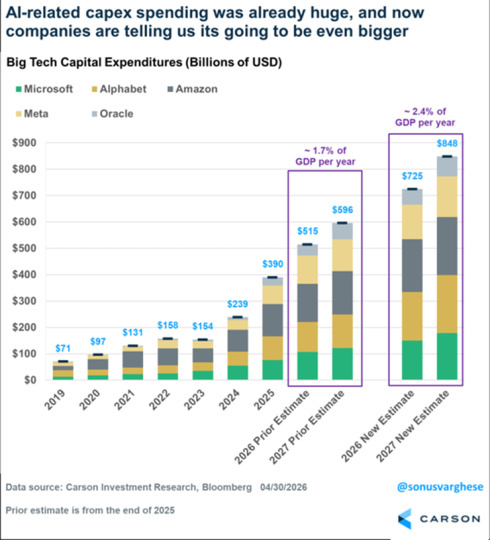

The bigger theme, however, remains macroeconomic. Because artificial intelligence is no longer just a stock market story. It has become a real economic force. Hyperscalers’ investments in AI infrastructure are contributing to economic growth and supporting demand for data centers, energy, networks, semiconductors, fiber optics, and construction. In some cases, a meaningful share of US GDP growth can be linked directly to this capex cycle.

This helps explain why the US economy continues to hold up despite high oil prices, elevated interest rates, and weak consumer confidence.

In summary, the overall backdrop remains constructive, but not straightforward. Equities continue to find support in earnings, nominal growth, and structural investment trends — particularly those tied to artificial intelligence. At the same time, however, the bond market is sending a signal that should not be ignored: persistent inflation, elevated oil prices, and large fiscal deficits require a higher risk premium.

This is not a sign of panic, but rather a call for discipline. Markets may still move higher, but they will require stronger confirmation and a much greater degree of selectivity.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.