The rally is holding up. Complexity is increasing.

21 May 2026 _ News

The market is at record highs, but it would be a mistake to pretend that the message is simple, because it is equally true that the broader context is becoming increasingly complex. Inflation continues to surprise on the upside, oil prices remain high, the Federal Reserve is less and less in a position to speak confidently about rate cuts, and the geopolitical landscape remains unstable.

Beneath the surface of a market that continues to rise, a range of very different signals are beginning to coexist: strong earnings, to be sure, but also expectations that are harder to beat; an economy that remains resilient, but with inflation that refuses to subside; and, above all, a balance that appears solid, but is likely more fragile than the record highs suggest.

However, the upturn still rests on three fairly solid pillars.

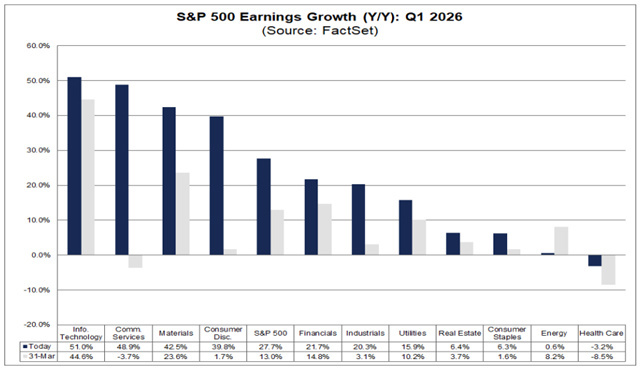

The first pillar, of course, is profit.

The first-quarter earnings season was simply exceptional. More than 80% of S&P 500 companies beat earnings estimates, roughly 80% also exceeded revenue expectations, and overall earnings growth rose by nearly 28% year-over-year—the strongest performance since 2021.

This is the true foundation of the current market. We’re not talking about a rally based solely on hype, but about a market that continues to be supported by corporate earnings that are much stronger than expected.

The point, however, is that precisely because this quarter was so strong, the bar will be set higher from here on out. When analyzing year-over-year growth, the comparison base always matters: if earnings jump significantly today, that very high number becomes the new starting point tomorrow. And so, to continue showing the same growth rate, companies will have to perform even better starting from a base that has already risen significantly. In other words, the market is currently riding the wave of enthusiasm from an extraordinary earnings season, but maintaining this trajectory in the coming quarters will inevitably be more difficult.

The second pillar is the labor market.

For months, it was said that the job market was the real weak spot in the U.S. economy, but the latest data tells a different story. For the first time in nearly a year, the United States has added jobs for two consecutive months, the unemployment rate has remained steady at 4.3%, and, most importantly, layoffs continue to be limited.

This is an important development, because a resilient labor market means steady consumer spending, nominal incomes that continue to grow, and an economy that—while slowing down compared to the stronger growth rates of the past—is not entering a period of real decline.

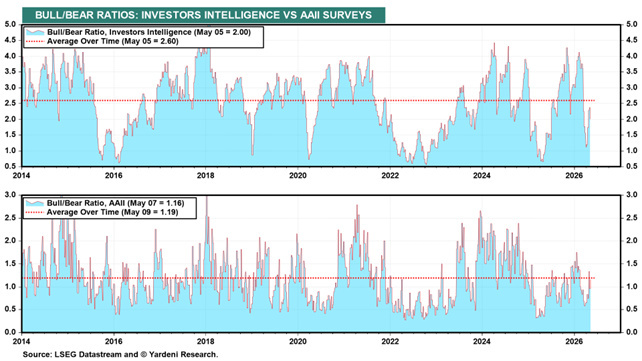

The third pillar—and perhaps the most interesting one—is sentiment.

What is surprising about this rally is that it continues to unfold in an atmosphere that remains closer to skepticism than to euphoria.

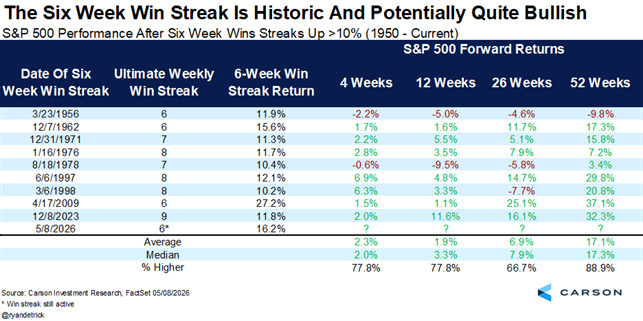

And from a contrarian perspective, that matters. The S&P 500 has risen for six consecutive weeks, marking one of the strongest streaks in recent decades. Historically, when the market posts six consecutive weeks of such strong gains, returns over the next six and twelve months tend to be above average.

But what is even more interesting is that this rally is not taking place amid widespread enthusiasm. Investors do not seem entirely convinced, consumer confidence remains low, and, more generally, the sense is that many still do not trust this rally. And this is a hallmark of bull markets that still have momentum: they thrive on skepticism, not euphoria.

That said, it would be wrong to turn this message into something naively optimistic. Because the fact that the bulls remain in control does not mean that everything is perfect.

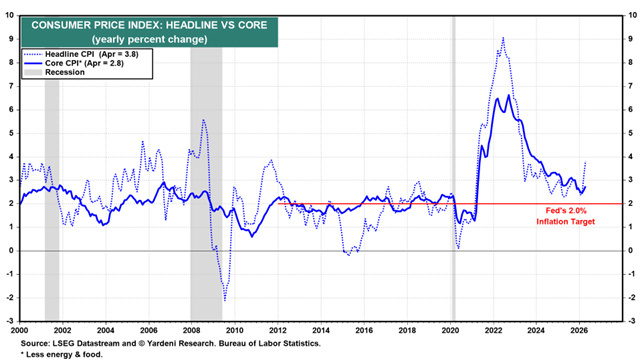

The most sensitive issue today is inflation.

April’s CPI and PPI came in stronger than expected. A significant portion of the increase came from energy, but that wasn’t the only factor. Transportation, logistics, and broader components of the basket are also showing signs of picking up again. As a result, while wages continue to rise, they are not keeping pace with inflation in real terms. This means that part of the resilience in consumer spending could become more vulnerable in the coming months.

Under normal circumstances, such a stable labor market coupled with such high inflation would be a strong argument for a more aggressive Fed. Instead, the central bank, at least for now, continues to effectively tolerate inflation well above its target. And it is precisely this combination—at least as long as it holds—that continues to be favorable for equities.

The problem is that this balance cannot be taken for granted indefinitely. Because if inflation remains high for too long, sooner or later the Fed will be forced to change its tone. It is probably not an issue that will play out in the very short term, but it is a tension that lingers in the background and that the markets will need to continue monitoring.

And this is where the bond market comes into play, having sent a rather clear message this week to both the Fed and U.S. policymakers. On the one hand, we still have high oil prices, unresolved geopolitical tensions, and the Strait of Hormuz, which continues to pose a real risk. On the other hand, U.S. macroeconomic data continues to show an economy slowing less than expected, with inflation, consumer spending, and the labor market still too strong to imagine a truly accommodative central bank.

The result is that yields have risen sharply, with the 10-year Treasury yield climbing back above 4.5%. I wouldn’t interpret this as cause for alarm, because at these levels, bonds are once again offering value, but it would be wrong to ignore the signal: the market is demanding a higher premium to tolerate high deficits and inflation that risks proving more persistent than expected.

What’s interesting, however, is that the stock market absorbed this movement without really breaking down. And that’s an important signal, because it tells us that bonds and stocks are currently viewing the same scenario through different lenses. The bond market remains focused on inflation, fiscal sustainability, and monetary policy. The stock market, on the other hand, continues to focus primarily on earnings, nominal growth, and major structural trends, starting with artificial intelligence.

There is another point worth emphasizing: while the market continues to rise, a significant portion of that growth is driven by semiconductors and the AI sector.

This doesn't mean the rally is fake. It does mean, however, that part of the lead is extremely strong and, in some cases, even extremely tight.

So the outlook remains positive, and the bulls still have strong arguments on their side. But at the same time, the market is entering a phase where a more selective approach is needed.

Today, the bulls remain in control. But to stay there for much longer, they will need these three pillars—earnings, employment, and widespread skepticism—to continue holding up. As long as that’s the case, the market may well remain bullish for longer than many expect. But from here on out, it will be less and less of a rally worth chasing.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.