Playing the commodity card with semiconductors

05 February 2021 _ News

The sector, one of the “thoroughbreds of 2021”, has cheaper valuations than the rest of the market, but is on course for strong earnings growth

Against a backdrop of economic recovery, it makes sense to look at the stocks and sectors that might benefit the most. They are the most cyclical sectors of the market and include commodity, which has been in the spotlight in recent months.

Indeed, after ten years of underperformance, the raw materials market could now be on course for a general upswing (to some extent this has already begun), further aided by the expected increase in the inflation rate.

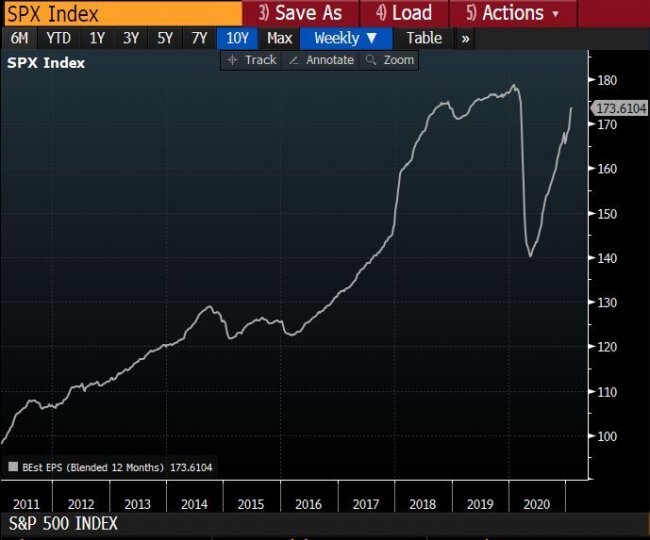

However, not all commodities are the same. Indeed, in order to ride this “new” trend, it might perhaps be worth tracking economic development and thus look beyond the more traditional indices, represented by precious (and non-precious) metals and agricultural raw materials, all capital intensive business areas. Today there is a significant change of direction towards increasingly less capital-intensive economies, which are not represented in the more traditional indices. In short, we should turn our attention to other commodities, such as wind power or even batteries. But there is one sector above all that Pharus believes will continue to set records: semiconductor. One only has to look at the growth of this sector over the last ten years, which reflects perfectly the general commodity index and is therefore experiencing continual growth. Its unbridled strength, combined with its cyclical characteristics, make this sector one of the most promising in 2021.

The key players in the semiconductor market supply the technology companies and are growth companies with sharply increasing profits. In an increasingly technological economy, it is inevitable that demand for these goods will continue to grow. The number of requests from the automotive industry, for example, is so high that demand is now outstripping supply.

Proof of this fact is provided by the companies themselves, such as the Dutch company ASML and TSMC (Taiwan Semiconductor Manufacturing Company), which have estimated growth rates for the coming years that were unthinkable up to yesterday.

Therefore, in the context of a digital economy, where technology is playing an increasingly significant role, it is worth asking whether looking at the more traditional commodities rather than focusing on “alternative” ones is really the right thing to do. From our point of view, it would make more sense to consider technology-related commodities such as semiconductors. This is a sector in which we have around 20% exposure through our Pharus Sicav Next Revolution fund. Valuations in this sector are cheaper than in the rest of the market and within this sector it is possible to select individual stories from which select stock picks.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.