The clamor of war versus the power of the economy

19 March 2026 _ News

The week on the markets was dominated by two very powerful forces that intertwined: on the one hand, the sharp resurgence of geopolitical risk; on the other, a U.S. macroeconomic landscape that, at least so far, continues to demonstrate greater resilience than expected.

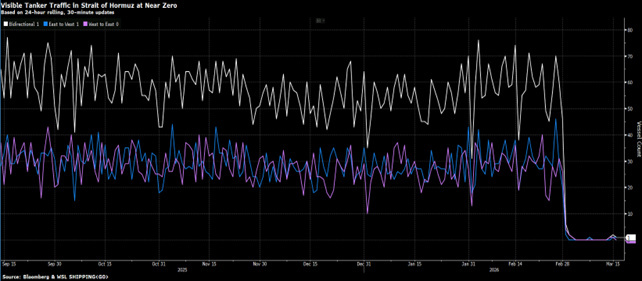

The starting point is oil. The movement we’ve seen in recent days wasn’t simply a rise in commodity prices, but a genuine supply shock. Crude oil recorded one of the sharpest weekly jumps in its recent history, driven by the fact that about 20% of global supply passes through the Strait of Hormuz, which, with the war in Iran, has effectively become nearly impassable for much of commercial traffic.

This is the real crux of the market right now. It’s not so much the conflict itself, but its immediate impact on energy prices—and thus on inflation expectations, interest rates, and ultimately stock valuations.

When a shock of this kind occurs, the market’s first instinct is always the same: a rapid rise in the risk premium. And indeed, we’ve seen oil climb toward the 0 mark, bond yields rise, the dollar strengthen, and the stock market enter its first real correction of the year. The S&P 500 has fallen more than 5% from its January highs, while the VIX has recorded one of its sharpest weekly spikes ever. These are movements that make headlines and inevitably fuel a sense of urgency.

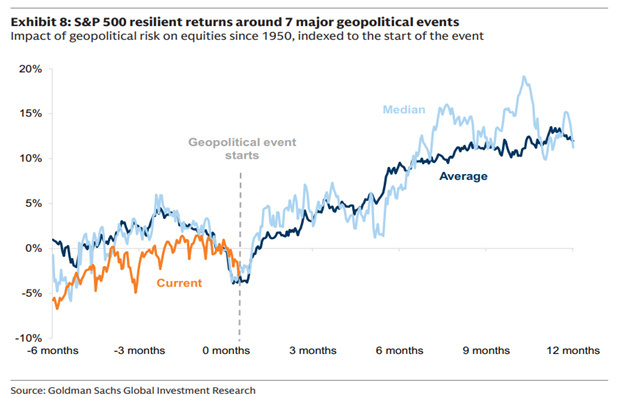

But this is precisely where we must be careful not to confuse the intensity of the movement with its duration. By their very nature, markets do not distribute returns in a linear or orderly fashion. Extreme events occur much more frequently than a simple normal curve would suggest. Yet the history of military conflicts teaches us that while the initial reaction may be very strong, it rarely reflects the final outcome for the investor.

This is a key point. Every war is different; every geopolitical shock follows its own course and has its own consequences. No one can say today how long the conflict will last, whether it will escalate, whether the Strait of Hormuz will remain blocked for weeks, or whether it will be reopened relatively quickly.

But we must not forget that financial markets and the real economy are not the same thing, even though they are often confused. Geopolitical or economic events are not automatically reflected in the markets as if in a mirror. Markets operate differently: they constantly try to anticipate the future; it is said that markets price in the future. This is why they react very quickly to news, but at the same time tend to absorb shocks faster than we imagine; once risks have been understood and incorporated into prices, markets are already looking ahead.

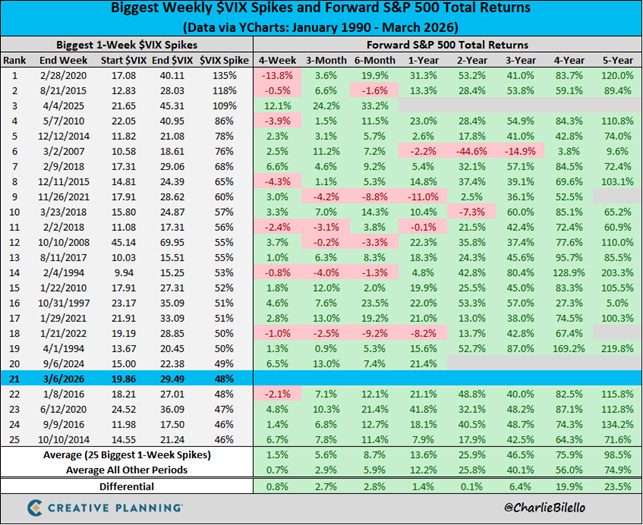

Based on the historical data analyzed in the chart (January 1990 – March 2026), it can be seen that periods of market panic, as indicated by sudden spikes in the VIX, have often coincided with extremely profitable buying opportunities for long-term investors.

Furthermore, financial markets do not merely reflect economic data. Above all, they reflect the way people and companies react to events. Ultimately, they represent humanity’s ability to adapt, innovate, and rebuild even after difficult times. It is no coincidence that it is often during times of crisis that new ideas and solutions emerge and the foundations for future growth are laid.

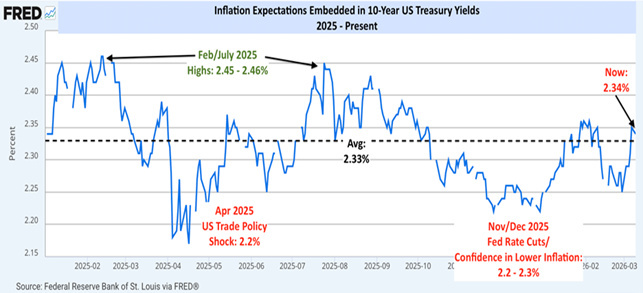

The issue, then, is not to deny the risk. The risk is real. If the conflict were to drag on, if oil prices were to remain high, if the closure of the Strait of Hormuz were to turn into a genuine structural disruption of global energy supply, the problem would become stagflationary. In that case, the Federal Reserve would find itself in a real bind: an economy that is slowing down but inflation that is rising again, driven by energy costs. And in fact, the market is already beginning to question this scenario. February’s CPI data, taken on its own, was reassuring: 2.4% headline, 2.5% core, a trend still consistent with a slow return to pre-pandemic levels. But that data was pre-war. The market is well aware that the impact of oil will be felt with a lag in the coming months, starting with gasoline, natural gas, and transportation, and extending to a long chain of industrial and consumer goods.

Yet—and this is where the picture is more nuanced than the headlines suggest—the U.S. economy continues to show remarkable resilience. Jobless claims remain subdued, layoffs aren’t skyrocketing, bank lending continues to expand, the services sector remains solid, and even the manufacturing sector, despite its vulnerabilities, is showing signs of improvement. Even the Atlanta Fed’s GDPNow—a sort of real-time measure of economic growth—has rebounded, helped by international trade data that was surprisingly better than expected.

In other words, while a war is being waged outside the United States that threatens one of the most vital arteries of the global energy trade, the American home front continues, at least for now, to hold firm.

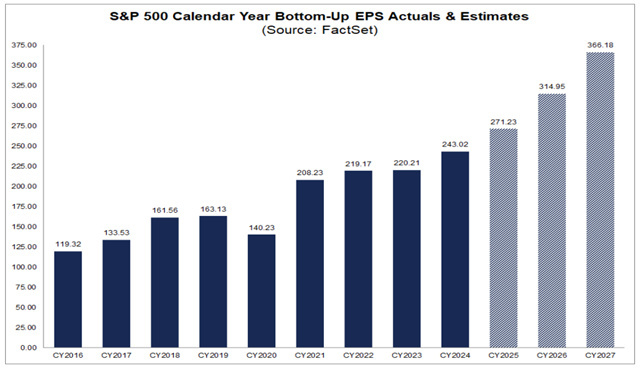

This is important for another reason as well: earnings. Because, ultimately, it is earnings that drive the markets over the medium term. And the bottom line today is that, despite the geopolitical noise, the earnings picture has not collapsed at all. On the contrary, companies’ ability to continue generating revenue, margins, and cash flow remains the key factor preventing the market from turning a correction into something more serious.

This is also why market corrections, however unpleasant, can have a beneficial effect: they bring valuations back to more sustainable levels and absorb some of the overvaluation that has built up over the previous months.

Meanwhile, another sector that seemed destined to deteriorate has instead begun to stabilize: the software sector. After weeks of anxiety over the idea that artificial intelligence might cannibalize a large portion of the SaaS industry, software ETFs are showing signs of technical resilience precisely during this period of peak geopolitical stress.

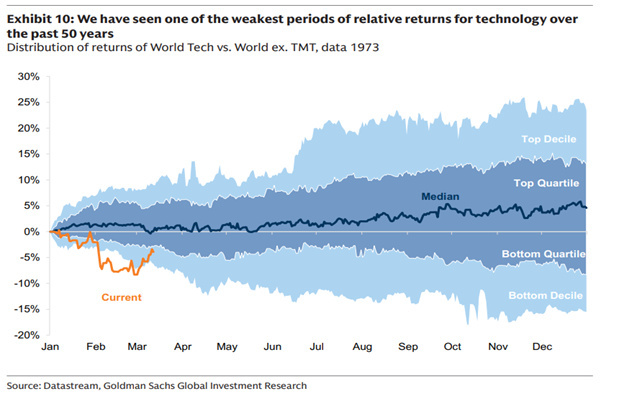

More broadly, the tech sector, too, is stabilizing after one of the most severe underperformances of the past 50 years. This is an interesting sign, as it suggests that the market is beginning to better distinguish between narrative and reality.

Ultimately, the market today is caught between two opposing forces. On the one hand, there is the noise of war, oil prices, inflationary risks, and the repricing of the risk premium. On the other, a U.S. economy that continues to demonstrate a surprising resilience, corporate earnings that are holding up better than expected, and a process of valuation readjustment that, however painful in the short term, can make the market healthier in the medium term.

Although the impact of this event on the global economy remains highly uncertain, experience from past historical events suggests that seeking refuge in liquidity is rarely the right strategy for managing geopolitical risks.

It is precisely at times like these that discipline matters more than forecasts. We need to cut through the noise, maintain a clear head, avoid sensationalist headlines, and remember that while markets react to news in the short term, in the long run they still follow earnings, growth, and valuations. History doesn’t tell us that things will always turn out well. But it does tell us that panic is almost always a poor advisor.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.