The market between energy shock and solid fundamentals

12 March 2026 _ News

The week on the markets was dominated by a factor that investors had not seen with such intensity for some time: the return of geopolitical risk. Oil rose sharply to over 0, while gas exceeded , and within a few days, inflation expectations began to move upward again. Suddenly, the market stopped discussing disinflation or artificial intelligence productivity, and the question became: are we entering a new energy shock?

The spark came from the conflict with Iran and, above all, from the most sensitive point in the entire global energy economy: the Strait of Hormuz. Although it has not been formally closed, maritime traffic has collapsed because the military threat has created a de facto blockade. Iran has declared that it is ready to attack ships passing through the strait, while the United States is considering providing naval escorts and maritime insurance to keep the route open.

This is the real crux of the conflict. Because a huge amount of oil—about 20% of the world's oil—passes through Hormuz, and any tension in that area immediately translates into a risk premium on the markets, with the ViX index rising above 30.

Here it is worth remembering a very simple but fundamental concept for those who invest in stocks. Ultimately, stock market prices are driven by two major variables. The first is corporate earnings. In the long term, earnings tend to grow: not in a perfectly linear fashion, but following a relatively predictable trajectory because they reflect the growth of the economy, productivity, and corporate revenues. The second variable, on the other hand, is the risk premium. In other words: how much the market is willing to pay for those earnings. This is what determines valuations, and therefore the multiples at which companies are traded.

And it is precisely this variable that generates most of the volatility in the markets. When uncertainty increases—as happens during wars or geopolitical crises—investors demand a higher risk premium to hold stocks. And when the risk premium rises, multiples compress and markets fall.

In other words, at times like these, it is not so much the trajectory of earnings that changes in the short term. It is the perception of risk. And this is precisely the mechanism that is driving most of the movements we are seeing in the markets today. Unfortunately, it is impossible to understand how the risk premium will evolve in the short term, which is why it is impossible to know how the markets will move in the short term.

It is a dynamic we have seen many times before: conflicts generate volatility in the short term, but markets tend to normalize once the news has been absorbed, unless the event truly changes the trajectory of the economy or earnings.

Much will depend on the duration of the conflict. If tensions continue or the Strait of Hormuz is actually blocked, the impact on energy prices could become more significant and also complicate the work of the Federal Reserve.

Meanwhile, another issue that had dominated the markets in recent months—the disruption caused by artificial intelligence—is beginning to find a balance. In previous weeks, many investors had begun to fear that AI could cannibalize the enterprise software industry.

But looking at the data and market prices, the panic seems to have subsided. Software sector ETFs found technical support even during the latest bouts of volatility, and several stocks have begun to stabilize. This suggests that investors are starting to distinguish between narrative and fundamentals.

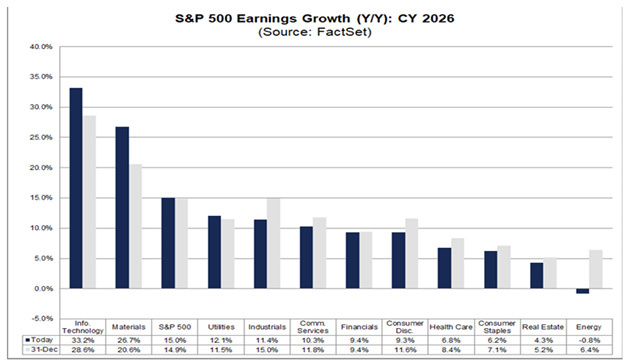

Ultimately, the market is currently navigating between two very different forces. On the one hand, there is geopolitical noise and the resulting volatility. On the other, an economy that continues to show surprising resilience. This resilience is not only evident in macro data, but also in corporate earnings, with estimates for the S&P 500 indicating earnings growth of around 15% in 2026, with expectations of expansion continuing into 2027.

This is an important factor, because ultimately it is earnings that drive markets in the medium term. And this is why, despite periods of tension and volatility, the underlying outlook for equities remains positive.

In fact, to be honest, this correction phase is also performing a rather healthy function for the market: it is bringing valuations back to more sustainable levels, reabsorbing some of the excesses that had accumulated in previous months, if not years. Movements like these often cause a stir in the short term, but in the long term they help to make the market more balanced and the foundations for the next growth cycle more solid.

The lesson, as is often the case, is that uncertainty creates short-term price movements, but rarely changes the direction of fundamentals unless it directly affects profits, consumption, or investment.

For this reason, at times like these, discipline counts more than forecasts and, above all, it is important to avoid being swayed by sensationalist headlines. No one has a crystal ball when it comes to the markets, and no one can know for sure how long the geopolitical tensions or the de facto blockade of the Strait of Hormuz will last.

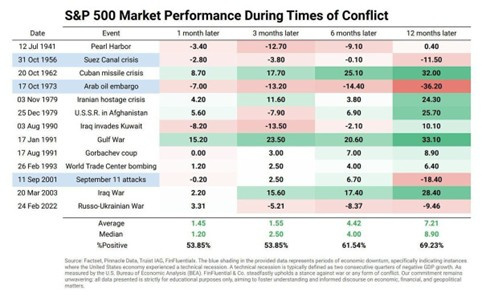

What we can do, however, is rely on history and statistics to rationalize the moment. Looking at previous geopolitical conflicts, a fairly clear pattern emerges: wars tend to generate volatility in the short term, but rarely change the trajectory of stock markets in the medium term.

If we analyze the main historical episodes, we see that twelve months after the start of a conflict, in 70-80% of cases, stock markets are positive, with returns substantially in line with long-term historical averages. This is an important reminder: in the short term, the market reacts to news, but in the long term, it continues to follow fundamentals. Bearish sentiment is likely to increase in the coming days, but this should not be misleading and should instead be exploited from a contrarian perspective to calmly increase equity holdings.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.