The rally that shouldn't happen

04 June 2026 _ News

If we had to find a phrase to describe this market phase, perhaps it would be this: the macroeconomic picture is more inflationary, but the economy isn’t slowing down.

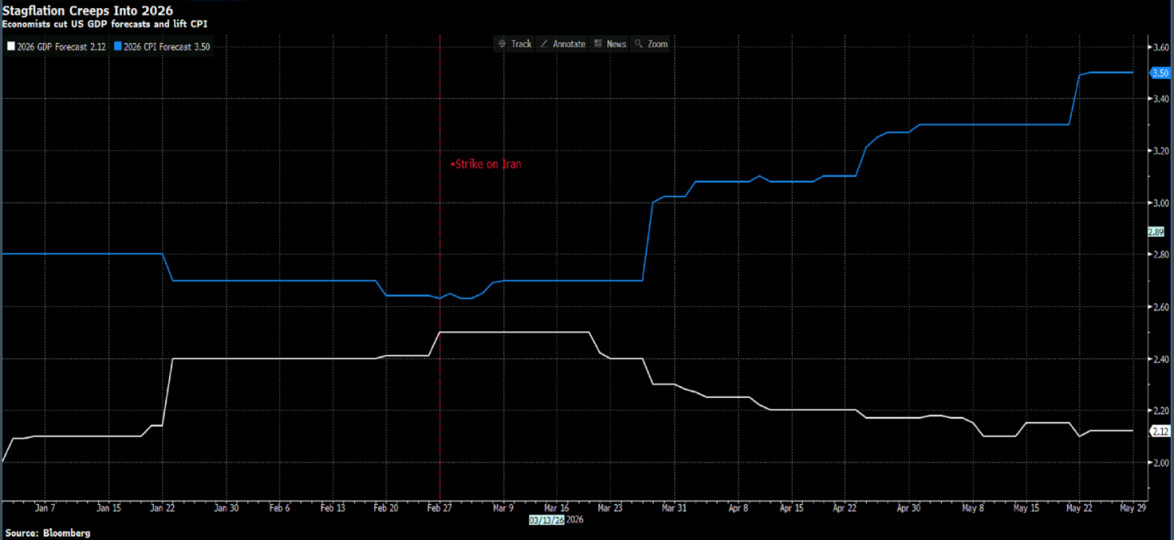

This is an important point, because in recent weeks the debate has focused almost exclusively on two risks: inflation on the one hand, and slowing growth on the other. And when these two elements are combined, the word that immediately comes to mind is stagflation. But, at least for now, the data do not tell a story of stagflation at all.

Instead, they tell a different story: an economy that is grappling with higher prices—driven primarily by oil costs and tensions in the Middle East—but which, at the same time, continues to demonstrate surprising resilience. Consumers are still spending, the labor market remains strong, the manufacturing sector is showing signs of improvement, and investments—particularly those related to technology and artificial intelligence—continue to underpin a significant portion of economic activity.

So the point is not to deny the risks, but to avoid confusing a rise in inflation with an immediate downturn in the economic cycle.

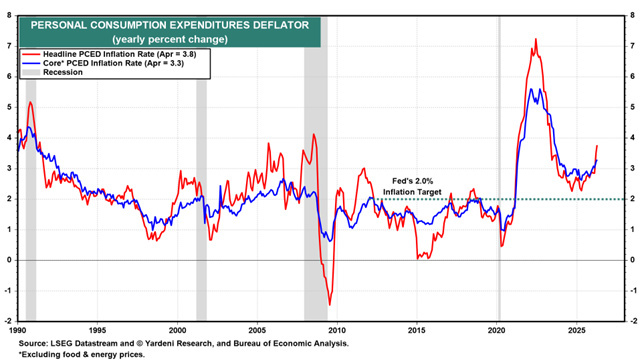

April inflation, as measured by the PCE, rose to 3.8% year-over-year, and even the core figure (which excludes the more volatile food and energy components) remains too high relative to the Fed’s target. This greatly complicates the central bank’s work, especially with Kevin Warsh having just taken the helm. Until a few months ago, the market was still anticipating rate cuts. Today, however, with more persistent inflation, volatile oil prices, and an economy that continues to hold up, that scenario is much less certain.

The point, however, is that the economy isn’t slowing down just yet. Consumers are feeling the pinch, as real wages are being eroded by inflation, but they continue to spend. The labor market is no longer as tight as it was in 2021–2022, but it remains solid: few unemployment claims, limited layoffs, and employment is still growing.

And this explains why the stock market has held up: if inflation rises while the economy collapses, the market is in trouble. But if inflation remains high in an economy that continues to grow, stocks can still find support in nominal growth, revenue, and earnings.

And that is exactly what we are seeing.

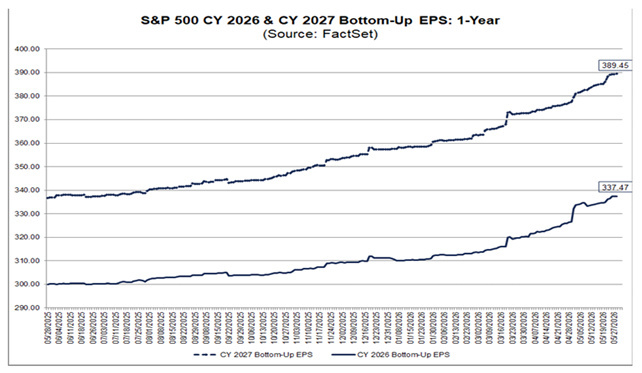

U.S. stock indices remain near their highs, despite a situation that, on paper, is certainly not without risks. The market continues to focus on earnings growth, the resilience of consumer spending, and the fact that the U.S. economy still appears capable of absorbing shocks that, at other times, would have triggered much more severe reactions.

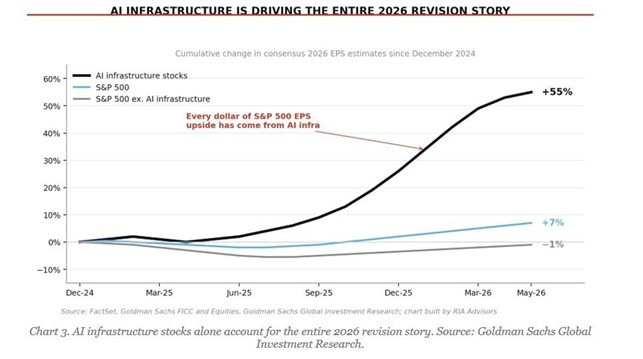

Manufacturing, which for months has been one of the weakest links in the economic cycle, is also showing signs of recovery. If you’re wondering why, the answer is simple… a significant part of this strength is linked to the cycle of investment in technology infrastructure, data centers, and artificial intelligence.

Artificial intelligence continues to be one of the major drivers of investment. It is no longer just a market narrative: it is real spending—on servers, data centers, chips, networks, energy, cooling, and construction. Every dollar of capital expenditure by hyperscalers translates into revenue for someone else in the supply chain. This is driving a significant portion of nominal growth and profits.

The AI cycle is becoming a real driving force for the economy, but at the same time it is increasing market concentration and making certain sectors much more vulnerable to potential setbacks.

And in fact, while the outlook remains positive, there are certainly risks involved.

The first factor is valuation. The S&P 500 is trading at high multiples, both in terms of price-to-earnings and price-to-sales ratios. This does not automatically mean that the market will fall. It does, however, mean that the margin of safety is narrowing. When valuations are high, any misstep regarding earnings, interest rates, or inflation is punished more severely.

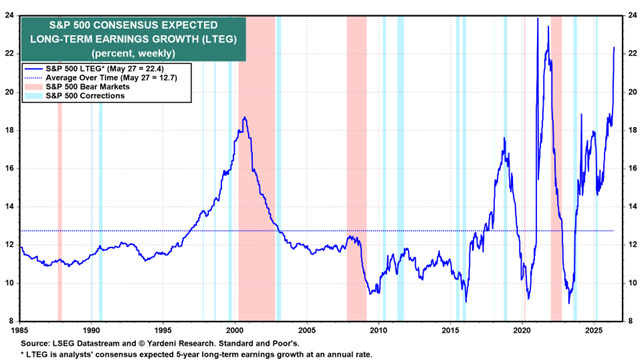

The second risk concerns earnings expectations. Analysts remain very optimistic about future growth, and some measures of expected long-term growth are now at historically very high levels. This can support the market as long as earnings continue to beat expectations. But it can also set the stage for a more volatile period if the pace of upward revisions were to slow.

The third risk remains geopolitical. The war in the Middle East is not over. The Strait of Hormuz remains the most sensitive point, because a huge proportion of the world’s oil passes through it. If tensions were to flare up again, oil prices could quickly rise above 0, increasing the risk of a scenario in which inflation and pressure on consumers become much harder to manage.

The fourth risk is concentration. A significant portion of the rally continues to depend on just a few stocks and a few sectors. When the market relies on a very narrow group of leaders, it can continue to rise for a long time, but it becomes more vulnerable if those leaders begin to lose momentum.

And finally, there is the more subtle risk: excessive enthusiasm.

The rally over the past few weeks has been very strong. The S&P 500 has posted a rare string of weekly gains, and historically, such streaks have often been associated with positive returns over the following twelve months. This is a positive sign. But in the short term, after eight consecutive weeks of gains, it is normal to expect a pause, a consolidation, and perhaps even some profit-taking.

The key takeaway, then, is not to chase every stock that has risen. Nor is it to sell everything just because the market seems overbought. The message is simpler: stay disciplined.

Reduce overexposure in areas where the portfolio has become too concentrated precisely because stock prices have risen sharply. Maintain liquidity to take advantage of any periods of weakness. Continue to maintain exposure to high-quality sectors, but without confusing the strength of the trend with the absence of risk.

In summary, this week brings us a market that remains resilient, yet is not without its contradictions and is caught between two opposing forces: on the one hand, inflation and higher yields; on the other, consumption, employment, and earnings that remain resilient. For now, the stock market continues to favor the latter, but the investor’s task is to remain flexible: to recognize the strength of the trend without ignoring where that strength could turn into vulnerability.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.