The strength of the market and the fragility of consensus

14 May 2026 _ News

If we had to sum up in a single sentence what the markets are trying to tell us today, it would probably be this: the bull market is still alive, but it’s becoming more demanding.

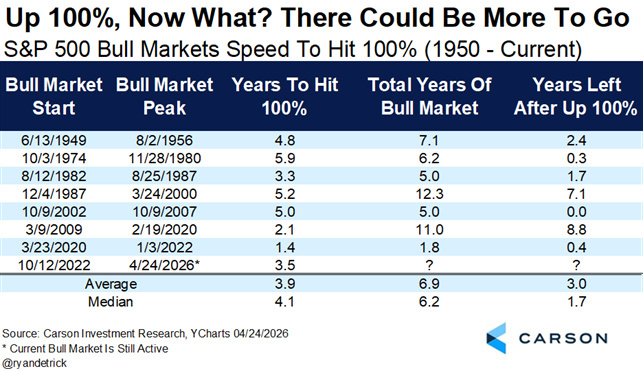

Because, on the one hand, the signs of strength are real, and it would be a mistake not to acknowledge them. April was one of the best months ever for U.S. stocks; the S&P 500 has more than doubled from its 2022 lows; the current bull market is now three and a half years old; and, historically, when a bull market gets this far, it very often still has a long way to go. In the past, bull markets that have passed their third anniversary have lasted, on average, several more years, and even after doubling from their lows, subsequent returns have often been very robust. In short, if we look only at long-term statistics, it is difficult to argue that this market is necessarily nearing its end.

But it would be just as wrong to stop there, because a much more subtle and far more interesting dynamic is taking shape beneath the surface.

The real question today is not whether the market has momentum. The momentum is there, and it’s clear. The real question is whether this momentum is widespread enough, healthy enough, and sustainable enough to hold up over the coming months.

Because the current rally has two very different sides. The first is constructive, almost inevitable: earnings continue to surprise on the upside, the labor market remains intact, consumer spending stays resilient, and the investment cycle in artificial intelligence continues to generate massive demand for capital, infrastructure, semiconductors, and computing power. The second, however, is more delicate: the market is becoming increasingly tight, increasingly concentrated, and increasingly dependent on a few big winners. And when this happens, the risk isn’t that the market will suddenly stop rising. The risk is that it will become much more fragile than the index suggests.

Let’s start with the positive news, because it deserves to be acknowledged honestly.

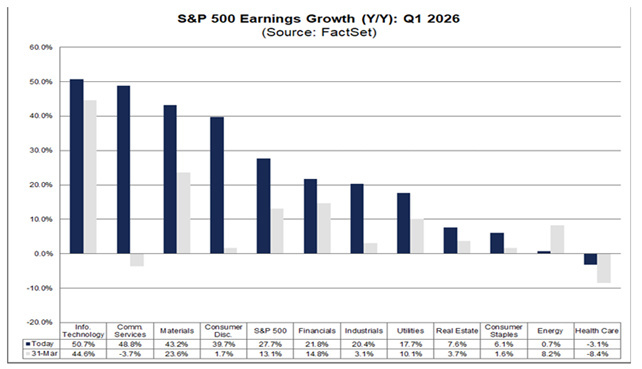

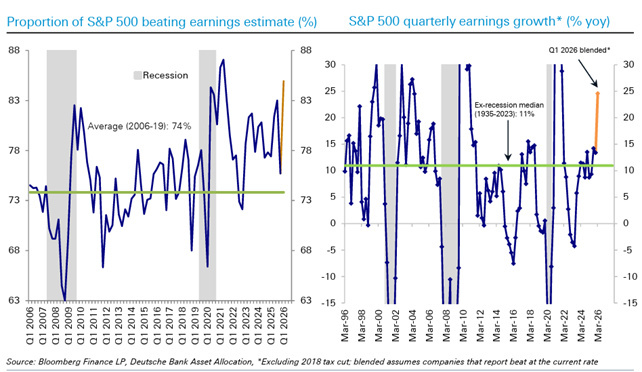

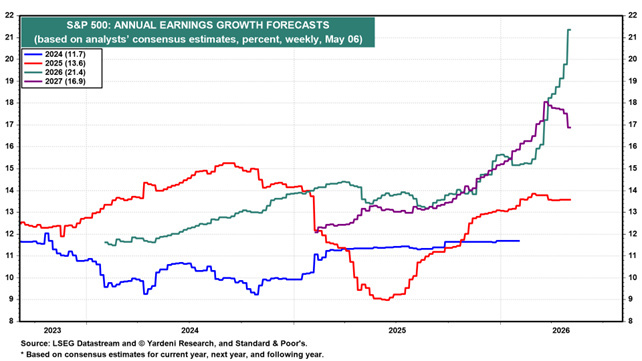

The first-quarter earnings season has produced figures that Wall Street rarely sees. About two-thirds of the companies in the S&P 500 have already reported their results, and overall earnings growth has risen to over 27% year-over-year—more than double what the market had expected at the end of the quarter.

The aggregate net margin has also reached levels not seen in fifteen years. So this is not a rally built on thin air. The market continues to be supported by strong fundamentals, and in particular by earnings growth that is much stronger than expected.

Furthermore, there is a second factor that supports this interpretation: upward revisions to earnings estimates did not stop even during the most tense weeks from a geopolitical standpoint. On the contrary, they continued to rise, and this is an important sign. It means that, while newspaper headlines were talking about war, oil, and the risk of stagflation, analysts continued to see companies capable of performing better than expected.

Even at the macro level, the picture remains less fragile than many make it out to be. If we really want to get to the heart of it, the real problem isn’t growth, but inflation.

Because while the labor market is holding up and earnings are surprising, real incomes are starting to be squeezed. Nominal income growth continues, but inflation is eating away at an increasingly large portion of that gain.

And it is precisely this combination that makes the market so difficult to read. Because historically, robust nominal growth coupled with high inflation tends to be a better environment for stocks than for bonds. Companies, at least to a certain extent, are able to pass on price increases and grow nominal revenues. Bonds, on the other hand, lack that flexibility. That’s why, despite high oil prices, a pause by the Fed, and inflation that remains a concern, the stock market continues to find support.

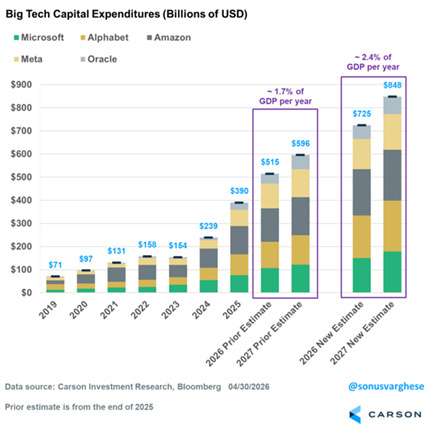

Added to all this is the major driver of the current phase: artificial intelligence.

We are no longer talking about a mere technological narrative. We are talking about a genuine investment cycle that is reshaping the market structure. The five major tech platforms are spending some 0 billion in AI-related capex by 2026, and estimates for 2027 continue to rise.

That is why semiconductors, network infrastructure, telecoms, and the entire “physical” side of the AI supply chain continue to outperform so decisively.

But this is precisely where the problem lies.

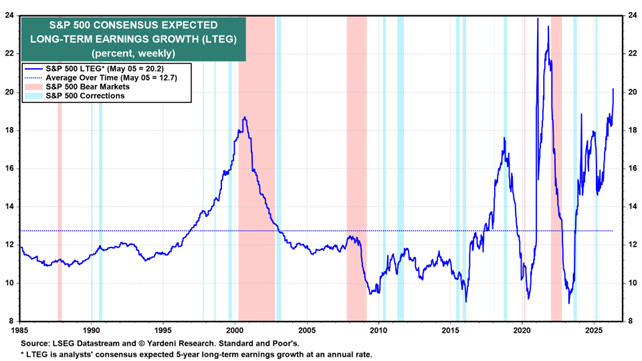

Long-term earnings growth expectations for the S&P 500 have now returned to levels not seen since 2000. And history teaches us one very simple thing: when everyone revises their forecasts upward at the same time, the next phase is almost never one in which companies surprise on the upside. It is the phase in which the market begins to fear the next mistake. Not because earnings are bound to collapse, but because even a mere slowdown in the pace of upward revisions is enough to trigger much more violent reactions.

When expected growth is +27%, a mere +26% is enough to shift market sentiment and trigger significant corrections. And this is where risk management comes into play.

Because while the market’s surface continues to look very reassuring, cracks are already visible beneath. The S&P 500 is hitting new highs, but the median stock in the index remains well below its peaks. The breadth of the rally is very weak. Market leadership is extremely narrow. Hedge funds are heavily exposed to momentum plays. Leverage is high. And we are entering that part of the year which, historically, is among the weakest: the May-October period, further compounded by the fact that this is a midterm election year—statistically the most volatile stretch of the entire U.S. political cycle.

This does not mean that a correction is certain. But it does mean that the risk-reward ratio is deteriorating—the very same point we highlighted at the beginning of the year.

Because in phases like this, the market risks becoming too complacent. Today we are not in a phase of panic; if anything, we are in a phase where investors seem to feel very comfortable again. And it is often precisely at these moments that risk tends to increase.

For this reason, in my view, the correct approach is not to suddenly turn bearish, but to return to being more disciplined and less lenient.

This does not mean exiting the market. It means recognizing that, at these levels, any further upward movement will need to be supported by more solid and timely confirmation. It means rebalancing portfolios, gradually reducing the most extreme concentrations, maintaining liquidity to take advantage of any pullbacks, and remembering that, when the market appears strong, risk does not necessarily decrease: often, on the contrary, it increases.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.