2023 is like a flashback to 2022

05 October 2023 _ News

Entering the final quarter of the year, we see an equity market that is showing more value than three months ago. This value creation has hit the so-called most interest rate-sensitive sectors, utilities-real estate and staples, as European and US government interest rates have risen sharply since June. These trends take us back to 2022, although with a different outlook. However, the result is the same, i.e. the creation of big opportunities in some parts of the market. It's a different outlook because the 2022 rate hikes were driven by inflation fears. But in 2023 it’s the upward revision of economic growth that is pushing up rates.

2022

Let's start with 2022, when inflation fears caused German interest rates to move from 0.8% in August to 2.4% in October, a 1.6% increase. In the same period, the US rate went from 2.4% to 4.2%, a rise of 1.8%. This change led equities to correct and they sank to their lows for the year, led by the technology sector. The Tech correction drove sector valuations at a discount, with the result that Tech ended up being worth as much in terms of price/earnings ratio as lower growth sectors such as Utilities and Staples (right-hand chart). This was a clear imbalance, arising from the rise in rates due to inflation fears. From here, opportunities then opened up for investors to buy the big tech stocks and this allowed them to outperform by more than 30% in 2023.

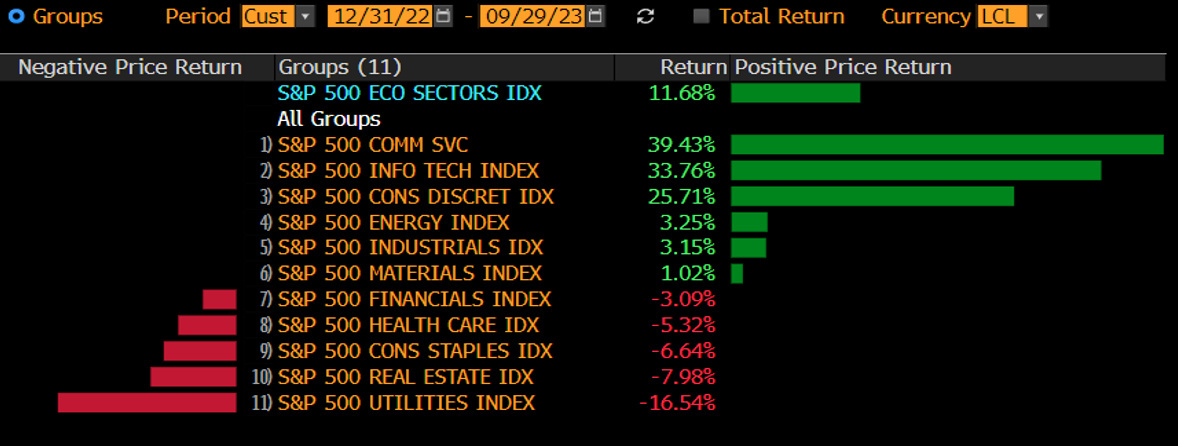

2023

Now we move on to 2023, with the German rate rising from 2.1% to 2.9% in the last six months, about 80 cents, and the treasury from 3.5% to 4.6%, a rise of about 1.1%. This rate change, driven by rising growth expectations, led the lower-growth, more stable sectors, which had held very well in 2022, to correct strongly. In fact, the market did not make much of a difference, leading defensive sectors such as Utilities and Staples to strongly correct and create great value. The market 12 months later has completely turned around, and, just as it was a struggle to buy Tech in October 2022, today the big struggle is looking at Utilities and Staples.

Conclusion

But a question springs to mind: is there any point in agonising over the reasons for the rises? Probably not. Rising rates hit tech last year, and this year they have hit other sectors. What drives this is value; rates have always hit the lower-value sectors the hardest. So we have a situation of equal and opposite excess compared to last year. This is why we mustn’t lose our bearings; as the great investors say, the investor's most important organ isn’t their brain but their stomach – and when it's backed by rational thinking it allows them to see opportunities. Indeed, we never tire of emphasising how value is very difficult to adopt, because it means buying when others are selling and selling when everyone else is buying. But it is the investor's best ally and also the best predictor of future performance. Because, when compared to the strategists of the various big firms, value is based on rationality, bows to no one and has no conflict of interest.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.