A relief rally, or the start of a new uptrend?

23 April 2026 _ News

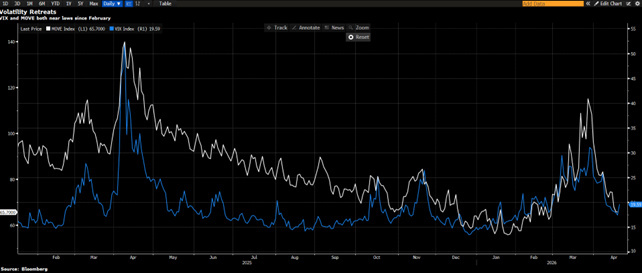

If we look solely at the index figures, the message would seem straightforward: the market has put its fears behind it. After weeks dominated by the war in the Middle East, soaring oil prices, and a continuous repricing of geopolitical risk, the S&P 500 has returned to all-time highs, the Nasdaq has set new records, and volatility has rapidly declined.

But as is often the case, the surface tells a simpler story than the reality.

Because what we’re seeing isn’t simply a return to calm. It’s a very sharp, very rapid rally, driven largely by relief. The market is pricing in the truce as if it were already a definitive solution. It is pricing in the reopening of the Strait of Hormuz as if the energy risk were now behind us. And above all, it is returning to buying risk at a pace that says much more about investors’ positioning than about the actual disappearance of the problems.

This is the key point.

In recent podcasts, we discussed how the market was extremely defensive. There were a lot of hedges, a lot of short positions, a lot of demand for protection, and a lot of fear—at levels typically seen near market lows. When the rally began to take shape, all these positions were unwound quickly. Short positions were covered, hedges were unwound, and the rally fed on itself. Then the most classic phase began: the chase. Those who had been left behind began chasing the move, while the indices approached their highs once again.

In just a few days, the market has almost entirely erased the risk-off sentiment triggered by the conflict. And when we see such rapid, steep rallies, we must always ask ourselves the same question: are we witnessing an improvement in fundamentals, or simply a sharp repositioning?

Probably, at least for now, the latter more than the former. Because if we look beneath the surface, the picture is still quite complex.

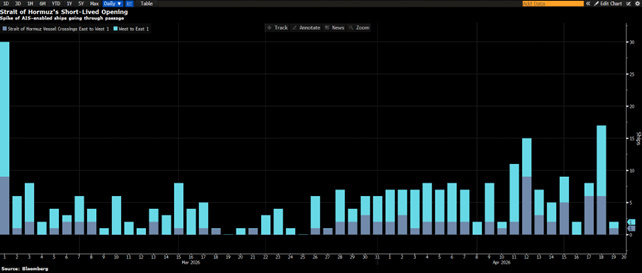

On the geopolitical front, for example, the risk has not disappeared. It has simply been put on hold. The ceasefire is fragile, traffic through the Strait of Hormuz has not yet returned to normal, and oil, despite having fallen sharply from its highs, continues to signal that the energy issue is not definitively resolved.

And this is a significant divergence: the equity market is pricing in an almost complete normalization, while the oil market remains much more cautious.

If real tensions were to flare up again, the sequence would be fairly clear: energy prices would rise again, inflation expectations would climb, central banks would be forced to maintain a restrictive stance for longer, and pressure would mount on bonds—and then, inevitably, on equities as well.

And yet, despite all this, the market continues to hold up very well. And this is where the second major theme comes into play: the resilience of the U.S. economy and expectations of strong earnings growth.

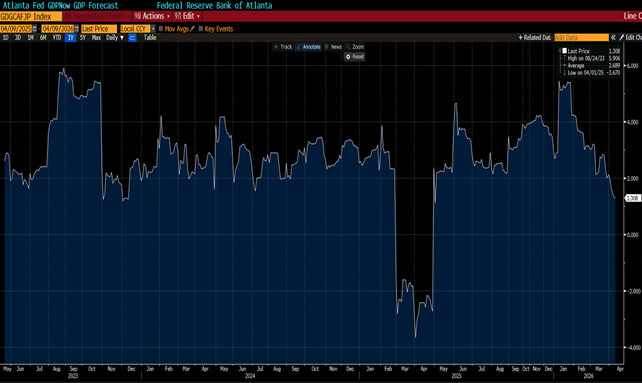

Because while the media buzz remains intense, the macroeconomic data continues to paint a picture of an economy that isn’t collapsing. Of course, not everything is perfect. The Atlanta Fed’s GDPNow has revised first-quarter growth downward, some construction data has been weak, and the slowdown compared to previous rates is evident. But we are not witnessing a break in the cycle. If anything, we are in a phase where growth is slowing down a bit, without, however, losing its underlying balance.

This is where earnings season comes into play—and I’d say it’s about time.

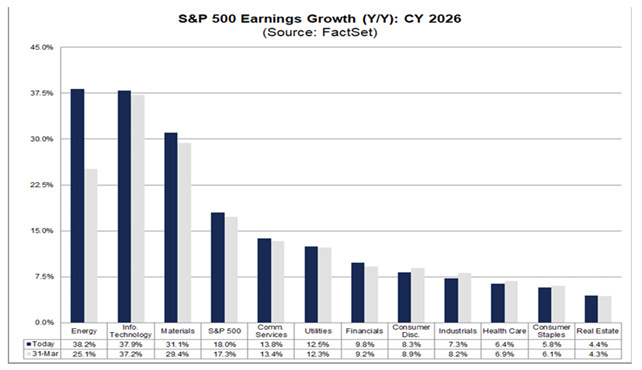

Expectations for the earnings season are anything but trivial. Consensus estimates remain very ambitious. The market continues to price in very robust earnings growth, driven largely by the technology and energy sectors.

But compared to the previous earnings season, those same expectations are now being priced in at lower multiples, which increases the likelihood that any positive surprises will be rewarded more readily.

I believe it is important at this stage of the market not to confuse the pace of the recovery with its sustainability.

The rally has been very strong, but it has also been heavily driven by technical factors, short covering, and the return of FOMO. This doesn’t make it a false rally, but it does make it more fragile. And so the real question for the coming weeks is this: will earnings confirm this enthusiasm?

In the end, it always comes back to this. In the short term, indices can be driven by geopolitical tensions, oil prices, market sentiment, positioning, and market narratives. But in the medium term, earnings remain the ultimate arbiter.

And that is why the phase that is now beginning is so important. The market has already gotten far ahead of itself. It has already decided that the war is, at least for now, a temporary blip. It has already decided that the U.S. economy is holding up. It has already decided that technology is once again the main driver. Now, however, we need confirmation.

So the point isn’t whether the rally was “real” or “fake.” The point is that from here on out, the market will need more than just geopolitical relief. It will need fundamentals to back up the rally.

If this happens, then the all-time highs could be surpassed in a more credible manner. If, on the other hand, earnings guidance begins to disappoint or geopolitical risks resurface, then this rally could turn into a new phase of consolidation.

In short: the market has shown impressive resilience, but this resilience stems more from positioning than from a full resolution of the underlying issues. The worst may be behind us, but we are not yet at the point where we can let our guard down completely.

For this reason, rather than chasing prices, it makes sense to continue to approach the situation with discipline: respect the rally, but without giving it a blank check.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.