Beneath the surface of the market, everything is changing

26 February 2026 _ News

If we look at the performance of the S&P 500 over the last few weeks, we might almost get the impression that nothing particularly significant is happening. The chart is orderly, realized volatility is compressed, and the average range of fluctuation is close to the lows of recent years. On the surface, it looks like a stable, almost motionless market, but those who stop at the surface risk missing the point entirely.

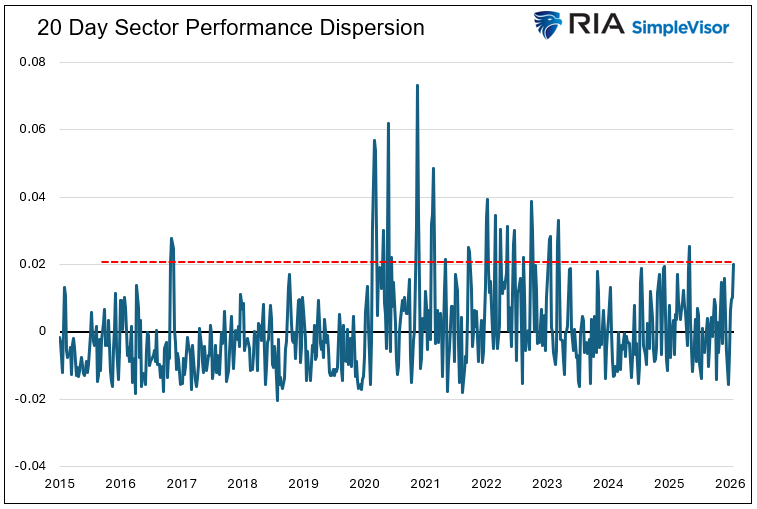

Because beneath this apparent calm, very deep currents are moving. The dispersion between sectors is among the highest in recent years, correlations have collapsed compared to 2025, and the returns between losing and winning stocks are widening significantly. This is not a market that is moving uniformly upwards or downwards. It is a market that is decisively reallocating capital, redefining leadership and priorities.

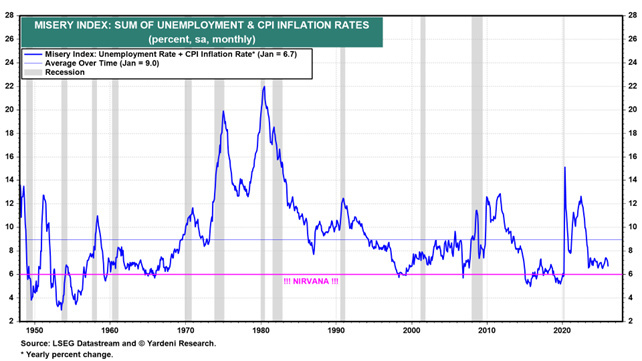

Taken in isolation, the macroeconomic context would appear reassuring. Unemployment stands at 4.3%, inflation at 2.4%, and the so-called “Misery Index” (simply the sum of inflation and unemployment) is close to levels that could almost be described as “Nirvana.”

The Fed has already cut 175 basis points since 2024, and today the real rate is back in line with its historical average. The minutes reveal a divided central bank, but one that is not concerned: there is no urgency for further cuts, and no signs of systemic stress.

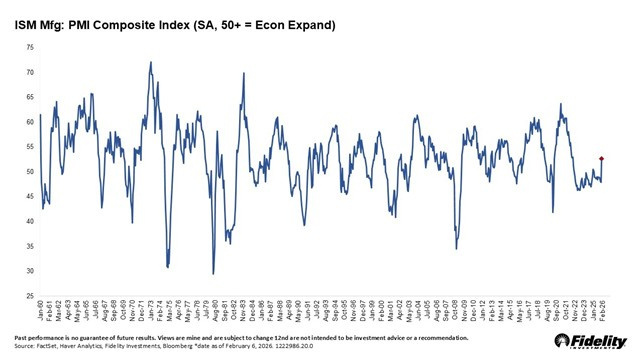

Yet something is changing. After one of the longest contractions in recent decades, manufacturing has returned above the expansion threshold. New orders have increased by almost 20%, a jump historically recorded in less than 5% of cases, providing a very strong signal compared to the “false starts” we have experienced in recent years. Apart from the consecutive recessions of the early 1980s, we have never seen the manufacturing sector stuck in contraction for as long as we have today. If this phase of weakness is finally coming to an end, it is very likely that we can talk about a cyclical upturn.

The current dynamics and what we might call “the Great Rotation of Valuations” should be viewed in this macro context. For years, leadership has been concentrated in large caps, in the Magnificent Seven, in the United States compared to the rest of the world. Now the market is rebalancing. Forward multiples in the technology sector have fallen from their year-end excesses; we are no longer talking about 30-35 times earnings but 20. The P/E ratio of the Magnificent 7 has been scaled back, while mid and small caps and markets outside the US are slowly gaining ground.

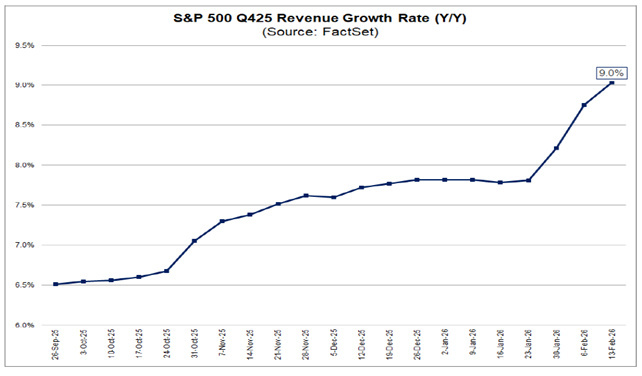

The very positive thing is that these dynamics are very orderly; we are not witnessing a collapse of technology, and we are not in a repeat of 2000. The substantial difference is that today profits exist and are growing. The latest earnings season showed double-digit profit growth and an acceleration in revenues that has not been seen for years. The fact that it is not only profits that are rising, but also turnover, is very supportive because it means that companies are actually increasing volumes and sales prices, not just cutting costs and working on margins.

The market has understood this well, and in fact is not denying growth, but simply recalibrating it.

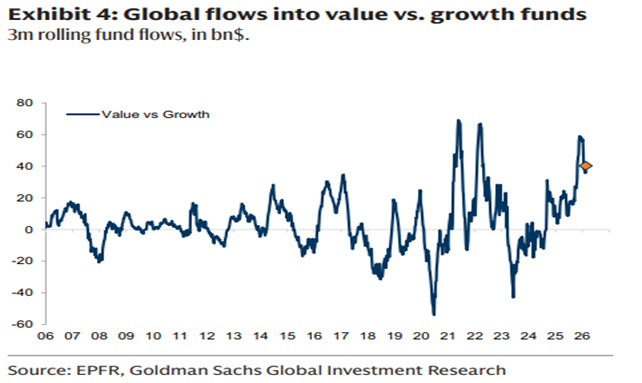

There is much talk of a rotation towards “value,” but the underlying reality hides an insidious paradox. Some stocks traditionally considered defensive are now trading at extremely high forward multiples, despite decidedly modest growth rates.

This is precisely where a silent repricing risk is accumulating. Buying a consumer staples stock at 40–45 times earnings means accepting a valuation premium that is difficult to sustain in the long term. If that multiple were to simply converge towards its historical average (close to 20x), the price would fall by close to 50%, even in the absence of a deterioration in corporate fundamentals.

This reminds us of something fundamental: the market is driven not only by logic, but also by narrative.

In Tech: When multiples rise, comparisons with the dot-com bubble immediately spring to mind. In “Safe” sectors: When valuations inflate in areas perceived as safe havens, there is almost total silence.

However, the chickens always come home to roost. While some “defensive” segments (only on paper) are now most exposed to a violent repricing of multiples, the Tech and Growth areas are beginning to deserve serious reconsideration.

We explored this topic in depth in the latest Fuoriclasse newsletter. You can read the full analysis by signing up for free at www.fuoriclasse.it.

What makes this phase fascinating, however, is that it does not resemble a crisis at all. In real crises, correlations explode, everything falls together, and dispersion is reduced because risk is sold en bloc. Here, the opposite is true: correlations are low, dispersion is high, and capital moves selectively. This is typical of transition phases, not collapse phases.

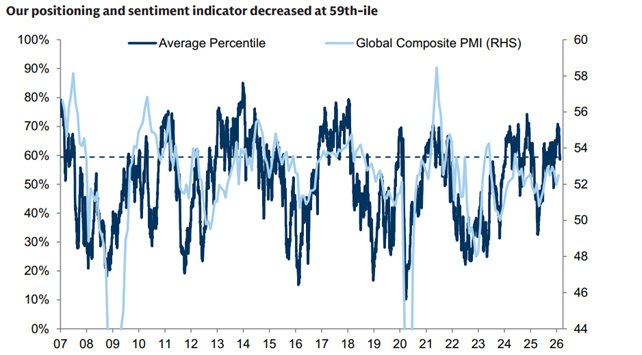

However, there is one factor that should not be ignored: complacency. Sentiment indicators remain relatively high, making it plausible that the first part of the year will be more irregular, with sudden movements and abrupt changes in leadership.

Ma allo stesso tempo, gli utili stanno accelerando insieme all’economia, il manifatturiero sta migliorando e gli indicatori di sorpresa economica stanno tornando positivi.

Il quadro, quindi, non è fragile. È complesso. Ed è proprio questa complessità che richiede disciplina.

Se guardiamo solo l’indice, vediamo calma. Se guardiamo sotto la superficie, vediamo una riallocazione di capitale che potrebbe ridefinire le gerarchie per i prossimi anni. Non è una battaglia tra growth e value, non è una guerra tra Stati Uniti e resto del mondo. È un processo di riequilibrio dopo anni di concentrazione estrema.

Il mare sembra piatto, ma le correnti si stanno muovendo con forza. E in queste fasi non vince chi osserva l’onda più visibile, ma chi capisce in che direzione sta andando la corrente invisibile.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.