Geopolitics and AI: the market recalibrates risk

05 March 2026 _ News

Geopolitical risk returns to the markets, with the conflict between the United States/Israel and Iran entering a more intense phase: Washington has announced that bombing will continue, while Tehran has officially closed the door on direct negotiations. The most sensitive issue remains the Strait of Hormuz, through which about one-fifth of the world's oil passes, with traffic slowed and maritime alert at the highest levels.

The markets' reaction has been typical of periods of tension: the dollar and gold are up, oil is under strong upward pressure, equities are more fragile, and the VIX index is rising.

We are not in a phase of systemic panic, but the real risk is not only military: it is energy-related and inflationary. A prolonged escalation would bring the issue of energy prices back to the forefront and, consequently, that of monetary policy. Meanwhile, Treasuries are recording one of their best months in the last year.

At the same time, another source of uncertainty continued to weigh on the market: the debate over the impact of artificial intelligence on business models. A report by Citrini Research reignited fears that AI is not only a productivity tool, but could structurally compress the value of intellectual work, professional services, and entire financial segments. Software, private equity, wealth management: several sectors have been repriced based on this narrative.

Yet, as often happens, the market does not remain anchored to a single narrative for too long. All it takes is a change of perspective, a piece of data, a comment, to quickly shift the balance between fear and rationality.

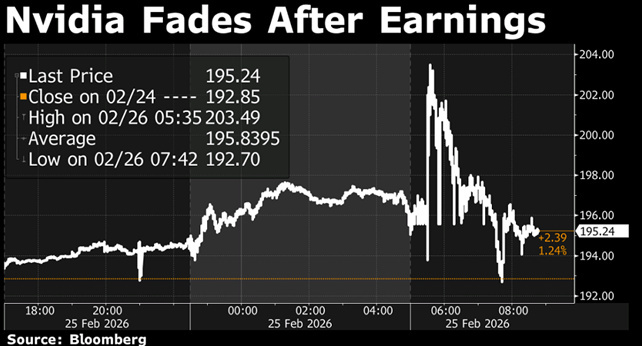

One of the most anticipated events of the week was Nvidia's quarterly report, which exceeded estimates, but the stock fell 5%.

The market, struck by a sort of “fear of AI,” fears that escalating capital expenditures and uncertainty about monetization are turning euphoria into potential systemic risk. Expectations were extremely high: to sustain further gains, a solid quarterly report was not enough; a further upgrade of the forward-looking narrative was needed, and this was lacking.

In an extensive interview with CNBC, the CEO dismissed as illogical the idea that AI could replace traditional software. However, investors remain cautious: the sector's growth trajectory appears increasingly dependent on debt-financed investment rather than organic cash generation.

Meanwhile, Meta has announced a 0 billion deal with AMD for AI-dedicated chips. The signal that emerges is different from the more extreme narrative: artificial intelligence does not indiscriminately replace existing business models, but tends to integrate into business processes, acting as an enabling lever and operational partner rather than a destructive force.

Anthropic has clarified that its tools will be used alongside existing software, not necessarily in place of it, and the market has reminded itself that the story is more nuanced than it appears and that perhaps the panic of the previous days was excessive.

Meanwhile, the macro picture remains surprisingly stable. Initial jobless claims remain low, at around 210,000. Inflation continues to move slowly in the right direction, although it remains above the 2% target. The Fed appears set to keep rates in their current range for now, with the market pricing in one or two cuts during the year. Economic growth, according to the Atlanta Fed's GDP now, stands at 3%.

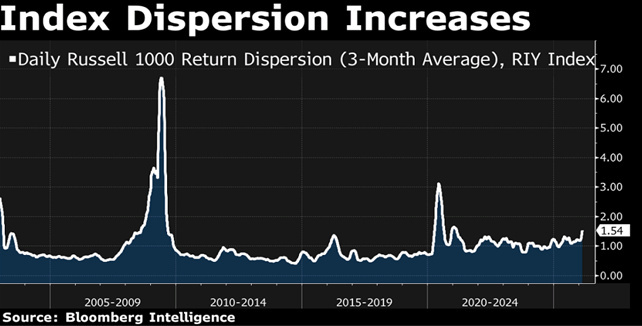

If we broaden our view of the markets, we can say that the bull market is still intact, but it is aging. Leadership is broadening. In recent months, the equal-weighted index has outperformed the magnificent seven, a rare event in recent years. The expansion has been benign so far: it has not been a rotation driven by the collapse of the leaders, but a gradual recovery of the rest of the market, which is to be seen as very positive.

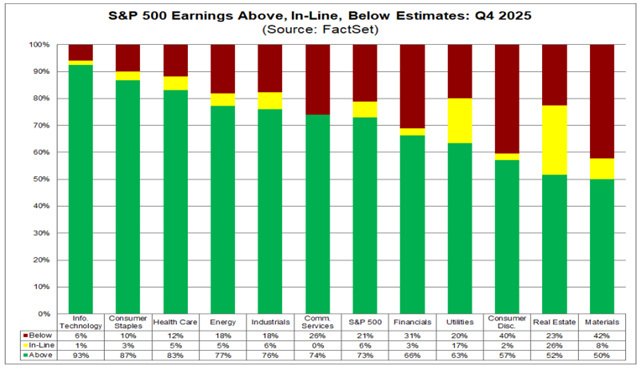

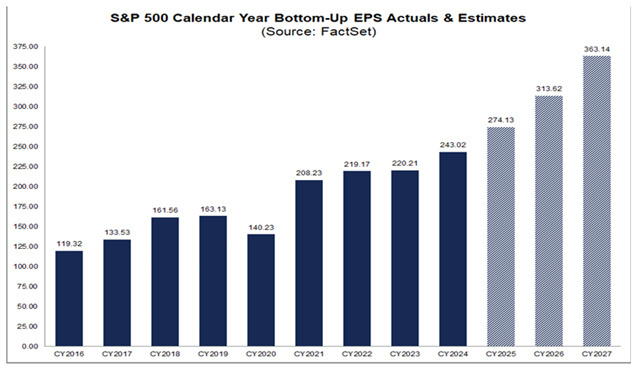

Earnings are supporting this momentum, with approximately 75% of companies beating estimates in the fourth quarter, with significant positive surprises and the S&P 500 price/earnings ratio not expanding further.

Significant acceleration in growth is also evident at the global level. Emerging markets are experiencing more dynamic earnings growth than the United States. European and emerging market equities are benefiting from a favorable combination of rising dividends and lower valuations. This is a process of convergence, not a flight from the United States.

The market, therefore, is simply redefining the price of risk, in an assessment context that until a few months ago was certainly very challenging, but we highlighted this several times last year.

And let's return to AI.

The so-called “AI Destruction Syndrome” has affected several industries. But at the same time, job openings for software engineers are on the rise, new applications for businesses have reached record levels, and many companies are integrating tools such as Claude into their daily workflows to increase productivity, not to replace entire teams.

Fear is understandable. Every major technological revolution generates fears of destruction. But history teaches us that the impact is often more transformative than terminal.

The key point at this stage is that the market is trying to understand who will be able to invest effectively, who will be able to finance this transformation without compromising their financial stability, and who risks being left behind.

Volatility is unlikely to disappear. Investors will continue to buy market corrections, and as long as earnings support the market and the expansion remains orderly, the bull market still has solid foundations.

It is no longer a market driven solely by enthusiasm. It is a market that weighs, measures, and compares.

The question is no longer whether artificial intelligence will change the world. The question is who will be best able to adapt as it does. And that is where the next phase of the market will be played out, which we are actually already experiencing.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.