High oil prices, a steady Fed, a strong market: why?

07 May 2026 _ News

If we were to judge solely by the headlines, one might almost conclude that the market is reacting irrationally. On the one hand, there are still many unknowns, with the geopolitical situation far from a real solution. On the other hand, however, the stock markets continue to show remarkable strength, with the S&P 500 and the Nasdaq near all-time highs.

If there’s one thing the markets have been showing us in recent weeks, it’s that reality is often much more complex than newspaper headlines suggest.

Because if we were to stop at the surface, the picture would seem almost contradictory. On the one hand, we have oil prices that remain high, the Strait of Hormuz that is still essentially blocked, a Federal Reserve that isn’t cutting rates, a war that continues to loom in the background, and an earnings season that, at least in some cases, is revealing a market that is far less forgiving than in the past. On the other hand, however, stock indices continue to hover near all-time highs, as if the system as a whole were still managing to weather the storm of all this turmoil.

And this is precisely where the market’s message becomes interesting. Because it isn’t telling us that risks don’t exist. It’s telling us something more subtle, but also more important: at this stage, the dominant factor continues to be the trajectory of earnings.

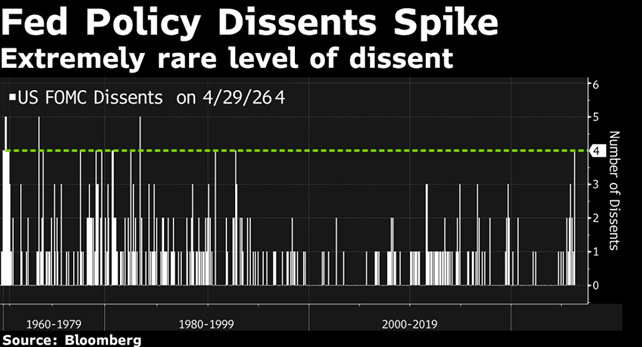

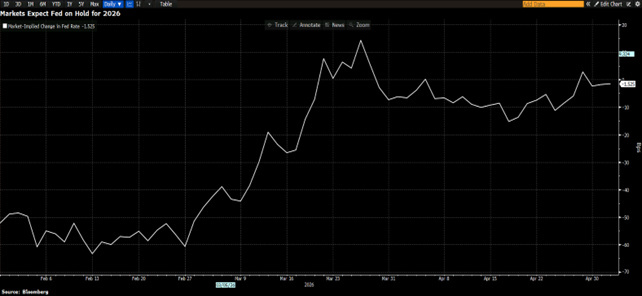

But let’s start with the Fed, because the outcome of its latest meeting was less straightforward than it might have seemed. Rates remained unchanged, as widely expected, but the figure that really matters was the level of internal division. The vote ended 8 to 4, the widest split in many years. This tells us that the central bank finds itself in an awkward, almost deadlocked position.

On the one hand, there is an energy shock that risks making inflation more persistent. On the other hand, the economy continues to slow less than expected and, for that very reason, does not give the Fed a strong enough reason to move quickly toward a more accommodative stance.

The result is that the Fed is holding steady; in practice, we’re in a wait-and-see phase, and the market seems to have grasped this quite well.

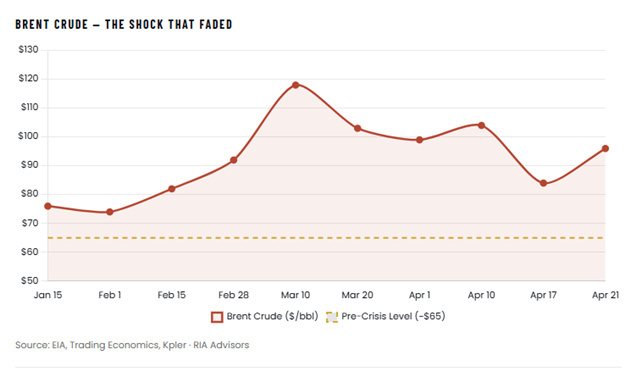

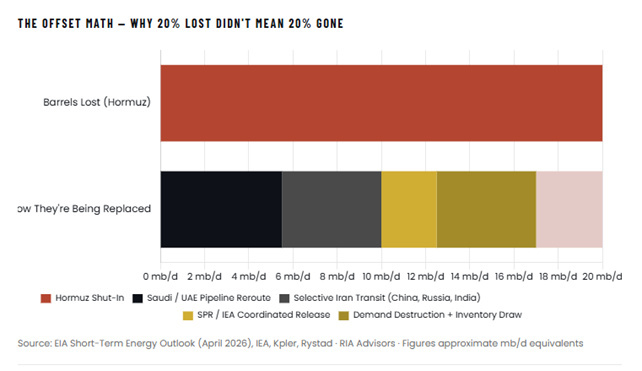

Even on the geopolitical front, if you will, the market is showing a greater ability to absorb shocks than expected. Tension over oil remains very real. Trump has further hardened his stance toward Iran, there is open talk of a prolonged blockade of the Strait of Hormuz, and crude oil has quickly returned to the 0 range. Yet, despite all this, the stock market is not behaving as one would expect in a classic stagflationary scenario.

The reason is that part of the shock has already been absorbed. Not all Middle Eastern oil has actually come to a standstill. A significant portion of the flows has been rerouted, some has been rationed but not completely cut off, strategic reserves have been tapped, and, above all, the United States is now much less vulnerable to an energy shock than it was in the past.

This doesn’t mean that risk doesn’t exist. It does mean, however, that the market has likely already factored in a significant portion of this risk and has begun to look beyond it.

And when the market looks beyond, it always comes back to the same thing: earnings.

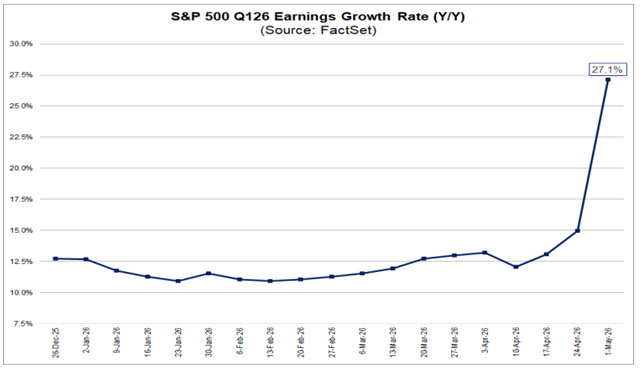

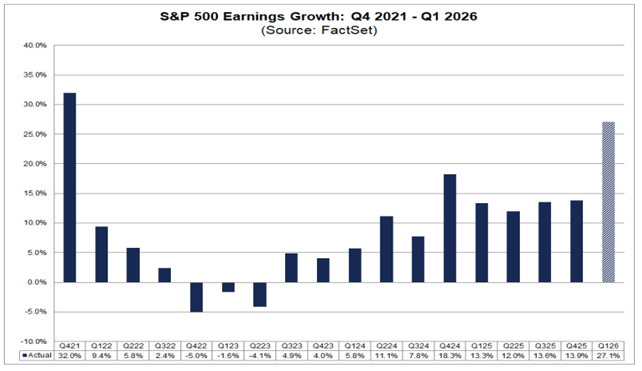

And this is precisely where this phase gets really interesting. Because earnings season, which is now in full swing, is telling us a very clear story. The numbers remain strong—often very strong—but the market has become much more demanding in how it interprets them.

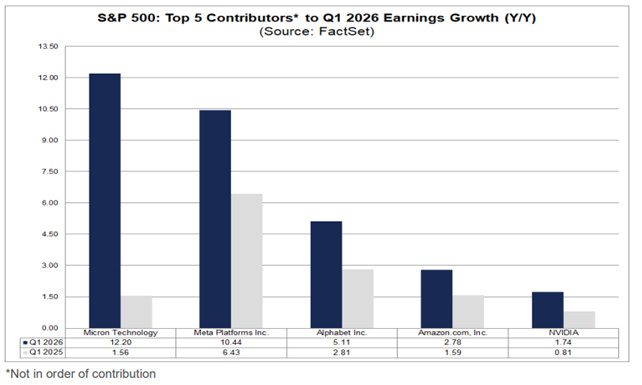

We’ve seen the results from giants like Alphabet, Microsoft, Amazon, and Meta, and overall, the numbers have been impressive. Amazon has accelerated further in the cloud. Microsoft has shown extraordinary growth in its AI division. Alphabet surprised with Google Cloud’s strong expansion. Meta has maintained extremely high margins while continuing to spend heavily. In short, from an industrial and operational standpoint, we’re talking about companies that continue to deliver top-tier results..

Yet the market is no longer satisfied with simply “beating” expectations. Today, it’s not enough to exceed expectations. Companies must do so convincingly, and above all, they must demonstrate that future growth justifies the level of spending these companies are undertaking.

This dynamic is even more evident in the rest of the tech sector. Software and the SaaS world continue to be treated with great caution. Conversely, the more “physical” and more directly monetizable parts of the AI cycle—hardware, semiconductors, infrastructure, and equipment—continue to be favored. This tells us that the rotation isn’t over. It’s simply becoming more refined.

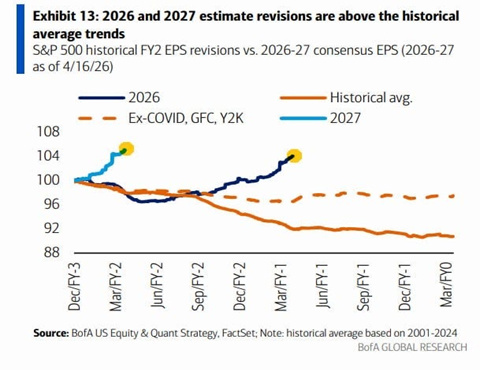

And this brings us to another key point. The market today is not driven by ever-higher multiples. It is driven by earnings. U.S. equities are not at record highs because investors have decided to pay any price just to remain exposed. In fact, in many cases, multiples have even compressed slightly. The rally has been driven primarily by rising earnings expectations and margins.

And that is precisely what makes the picture much less fragile than it might seem at first glance. As long as the earnings trajectory remains intact, the market can cope even with high oil prices, a Fed on hold, and unresolved geopolitical tensions. In this sense, the narrative isn’t winning. Fundamentals are winning—at least for now.

The question is no longer whether earnings will grow. The issue is whether they will grow enough to satisfy a market that has already begun to price in a great deal. And this is a fundamental distinction. Because a strong market is not necessarily a simple market. In fact, it is often the opposite: the stronger the market, the more selective it becomes, the less forgiving, and the quicker to reward those who truly convince and to punish those who even hint at uncertainty.

That is why the correct interpretation of this phase is neither that of the doomsayers nor that of the optimists. The market is not wrong to remain relatively calm about Hormuz. But it is not saying that everything is resolved either. It is simply doing what it always does: following the earnings trajectory as long as that trajectory remains credible.

The real question for the coming weeks, then, is not so much whether the market can still rise. The real question is whether earnings will manage to confirm a level of expectations that is becoming increasingly ambitious, just as part of the rally is concentrated in areas that are getting more and more crowded and stretched.

After all, this is where the real game is being played. The bull isn’t dead. But from here on out, momentum alone won’t be enough. We’ll need increasingly precise confirmation.

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.