Uncertainty and Pessimism: Why the Market Might Surprise on the Upside

26 March 2026 _ News

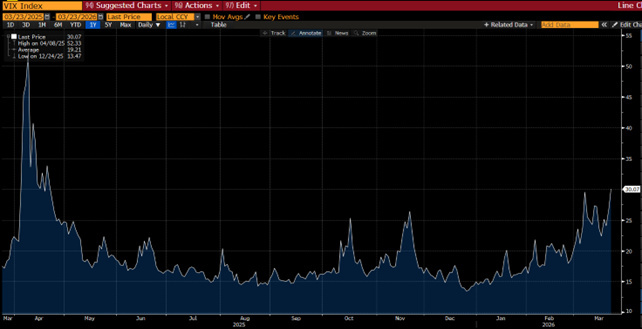

The week on the markets was dominated by a complex interplay of macroeconomic and geopolitical factors, with growing uncertainty and increased volatility at the center.

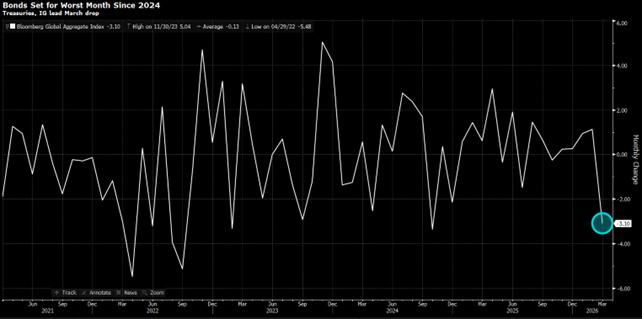

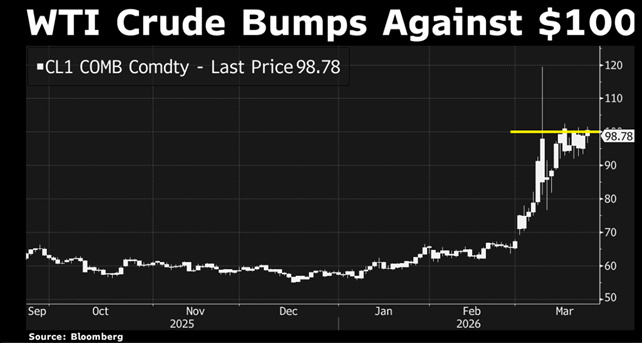

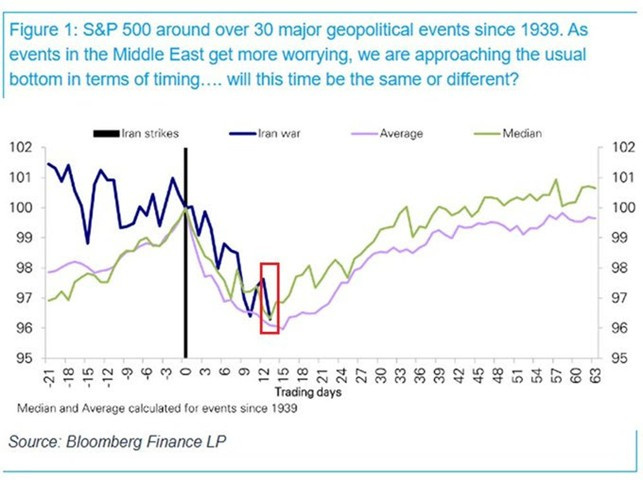

On the one hand, the conflict in the Middle East continues to be the main driver of volatility. The key issue remains the Strait of Hormuz, through which approximately 20% of the global oil supply passes. Tensions in that area have pushed the price of crude oil above 0 per barrel, immediately reigniting inflation fears and putting pressure on both stock and bond markets.

On the other hand, it was also a week in which the Federal Reserve found itself in an extremely delicate position. Few Fed meetings in recent history have presented the FOMC with a more unsettling set of mixed signals than those at the latest meeting, where the U.S. central bank kept rates unchanged in the 3.50%–3.75% range, but revised its inflation estimates upward to 2.7%, raising them by 0.3% compared to the December meeting, clearly signaling that the energy shock could slow the path toward bringing inflation back under control.

This has had a direct impact on the markets and on expectations regarding the future path of interest rates. Before the crisis in Iran, options markets indicated an implied probability of just 7% that the Fed would raise rates in 2026; now that figure has risen to 35%.

Rising interest rates also have significant implications for stocks: when the cost of capital increases, the present value of future cash flows decreases, which compresses valuations and causes stock prices to fall.

The Fed currently finds itself caught between two opposing forces. On the one hand, there is a potential surge in energy-related inflation; on the other, there are signs of an economic slowdown, weak growth, sluggish consumer spending, and a labor market that is beginning to lose momentum.

This is the classic “policy dilemma”: cutting interest rates to support growth risks fueling inflation, while maintaining a restrictive policy (i.e., not cutting or even raising rates) risks further slowing the economy.

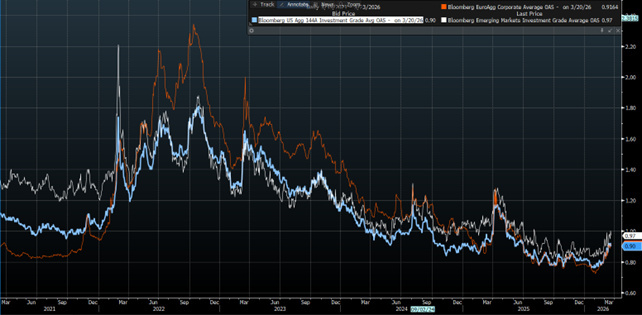

In this context, the markets are trying to price in a variable that, by definition, is unpredictable: the duration of the conflict. The longer the war drags on, the greater the impact on inflation, growth, and monetary policy. Everything hinges on the duration of the conflict.It’s a complex situation, and the markets are beginning to realize this; in fact, more technical but highly significant signals are starting to emerge. One such signal is the widening of credit spreads—that is, the rise in yields on corporate bonds.

This is an indicator that often goes unnoticed, but it is crucial. Because credit is the lifeblood of the economic system. When spreads begin to widen, as they are doing right now, it means the market is pricing in increased risk and tighter financial conditions. Historically, these dynamics should never be underestimated, because they tend to foreshadow more challenging times for the stock market. Very often, major stock market declines have been preceded by a decline in the corporate bond market, and analyzing these dynamics would therefore suggest a potential cause for caution (although, as can be seen from the chart, the widening of spreads cannot currently be considered significant).

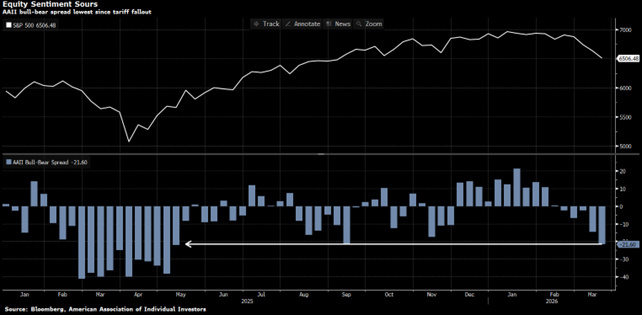

That said, however, we must avoid falling into a one-sided and pessimistic interpretation, and to do so, it’s worth taking a step back and looking at another key factor: market sentiment. Because beyond the news, what often really matters in the markets is how investors are positioned.

We find ourselves in a rather interesting situation today. The level of pessimism is very high.

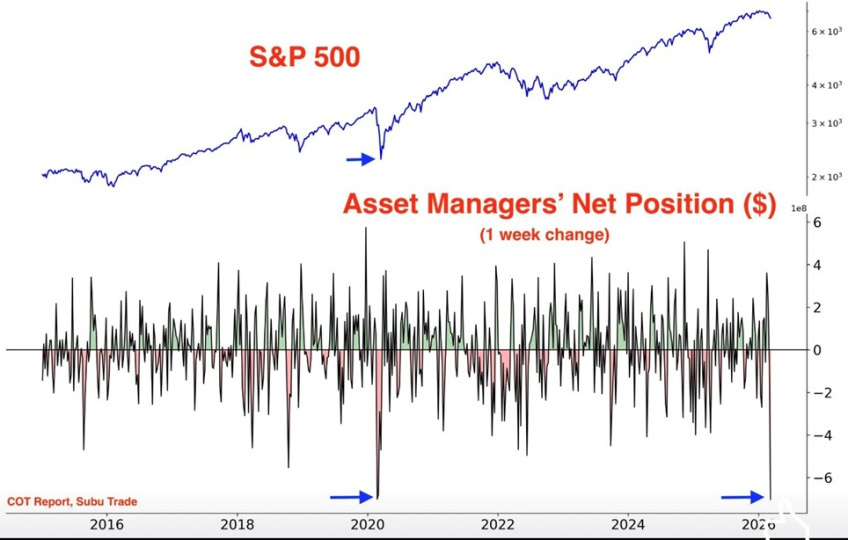

Historically speaking, this is a signal that should not be ignored. Sentiment indicators such as the Fear & Greed Index are at levels of extreme fear, investor surveys show a clear prevalence of bears, and asset managers’ exposure has fallen to its lowest levels in recent months—meaning that institutional investors have already sold off a significant portion of their holdings and are already positioned for negative scenarios.

The key point is that when market sentiment becomes so skewed, it means that much of the bad news is already priced in. Markets don’t react so much to negative news in and of itself, but rather to the extent to which it surprises relative to expectations. And today, expectations are already very low.

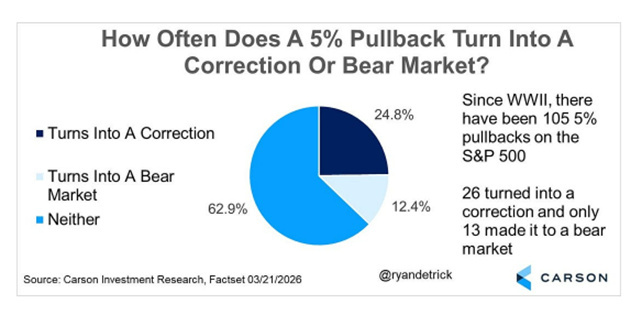

But instead of relying on gut feelings, let’s look at the data. As of today, the markets are down just over 5%. Since World War II, there have been 105 declines of 5%. Do you know how many of those turned into full-fledged corrections—that is, declines of more than 10%? Only about 25%.

And how many turned into bear markets—that is, drops of more than 20%? Just a little over 12%.

In other words: in 62% of cases, a 5% drop… is simply a 5% drop, and then the market starts to rise again. Yet every time, investors react as if it were the beginning of a historic crash.

This doesn’t mean that risks don’t exist. They certainly do. But the odds paint a less dramatic picture than people perceive.

Four years ago, Warren Buffett was asked what to do in the event of a world war, and he replied:

“Well, even if you tell me all that’s going to happen, I’ll still keep buying stocks. The only thing you can be fairly certain of is that if we were to enter a large-scale war, the value of cash would decline.

I mean, it’s happened in practically every war I’m aware of. So the last thing you’d want to do is hold cash during a war. You might want to own a farm, you might want to own an apartment building, you might want to own stocks… Over the next 50 years, you’ll be much better off owning productive assets rather than pieces of paper.”

This, of course, does not rule out further volatility in the short term. Markets could remain weak, and a more significant correction would also be natural, helping to bring valuations back to more sustainable levels.

At the same time, however, the fact that investors are already very defensive is a key factor: if even some of these uncertainties were to ease, everyone who has sold would have to rush to buy back in, helping to drive the market higher.

The real question, then, is not whether there will be volatility—that is inevitable—but whether this volatility will turn into something more profound, namely a structural deterioration in growth or earnings.

As of now, this is not the baseline scenario, so the conclusion is quite clear, and once again we can only agree with Warren Buffett: “I will continue to buy stocks regardless.”

The contents of this informative message are the result of the free interpretation, evaluation and appreciation of Pharus Asset Management SA and constitute simple food for thought.

Any information and data indicated have a purely informative purpose and do not in any way represent an investment advisory service: the resulting operational decisions are to be considered taken by the user in full autonomy and at his own exclusive risk.

Pharus Asset Management SA dedicates the utmost attention and precision to the information contained in this message; nevertheless, no liability shall be accepted for errors, omissions, inaccuracies or manipulations by third parties on what is materially processed capable of affecting the correctness of the information provided and the reliability of the same, as well as for any result obtained using the said information.

It is not permitted to copy, alter, distribute, publish or use these contents on other sites for commercial use without the specific authorization of Pharus Asset Management SA.